At $620.0B pre-move market value, ExxonMobil Corp. is among the largest firms in the cohort and carries disproportionate weight in market-value-weighted aggregates. Vote scheduled for 2026-05-27; results pending.

Controller & ownership

Diffuse / non-controlled

Ownership concentration data not yet documented for this firm.

Source: Widely held, no controlling shareholder

Vote outcome — reincorporation proposal

Approval standard: Per DEF 14A 0001193125-26-147614: favorable vote of a majority of votes cast; transaction effected through plan of merger under NJBCA Title 14A Chapter 10 + TBOC merger provisions. Meeting type: annual.

Vote totals not yet pulled. Awaiting EDGAR Item 5.07.

Visual evidence — event study around the March 10, 2026 announcement

Six chart-level views of the announcement-window data. Captions are verbatim from the underlying figures; underlying numbers come from xom_rerun_results.json (estimation window 2025-03-25 to 2026-03-09, 240 trading days; 21 energy-sector donors; SC top-3 weights CVX 0.55, EOG 0.20, SLB 0.09).

ExxonMobil tracked its energy-peer benchmark through the announcement

Pre-announcement tracking error = 0.77%. The two lines stay close through the announcement and after — that visual co-movement is the null finding.

Method

Synthetic control · 21-firm energy-sector donor pool · normalized to 100 sixty trading days before the announcement.

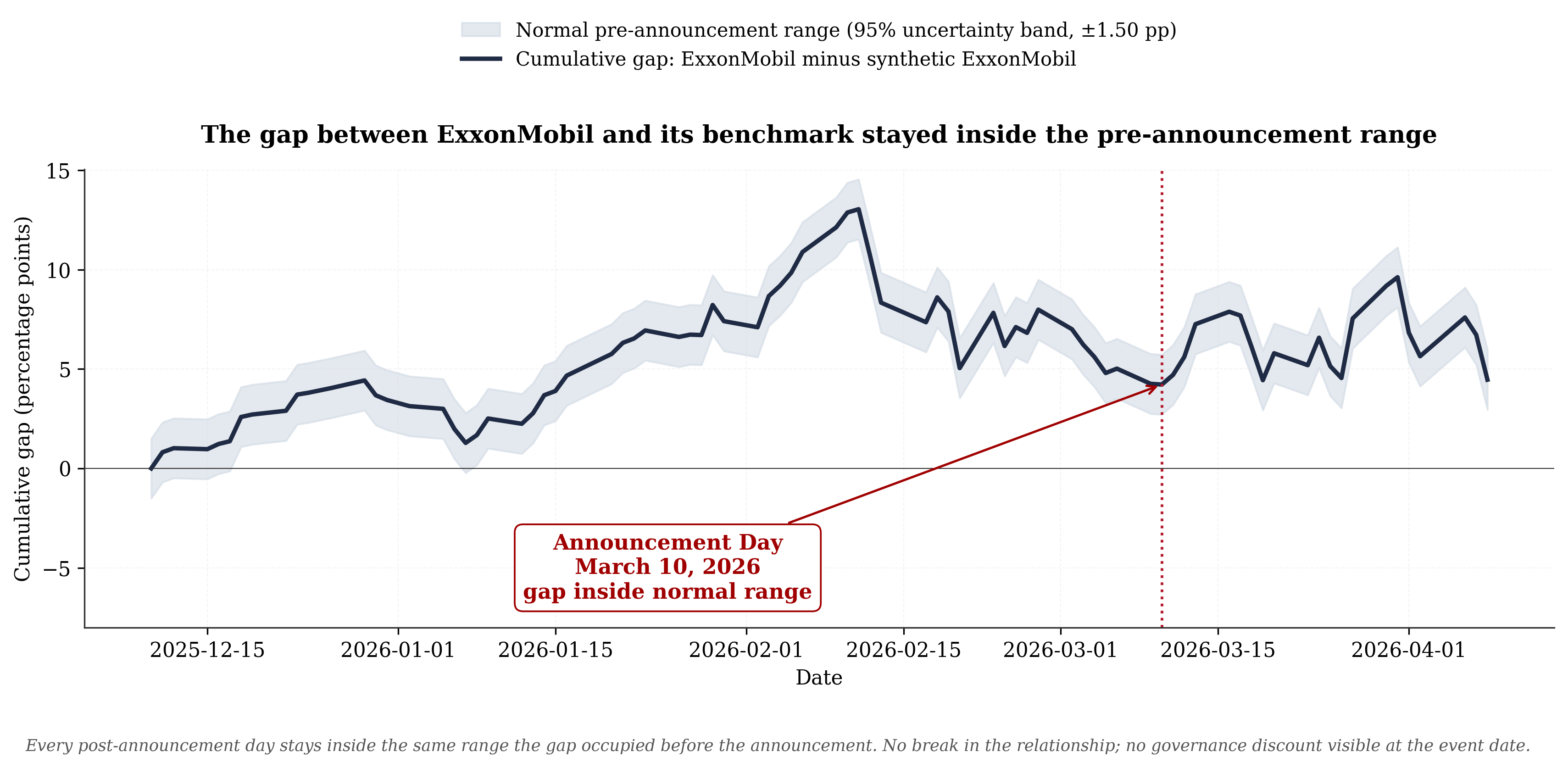

The gap between ExxonMobil and its benchmark stayed inside the pre-announcement range

Every post-announcement day stays inside the same range the gap occupied before the announcement. No break in the relationship; no governance discount visible at the event date.

Method

Cumulative ExxonMobil-minus-synthetic gap with ±1.50 pp 95% pre-announcement uncertainty band.

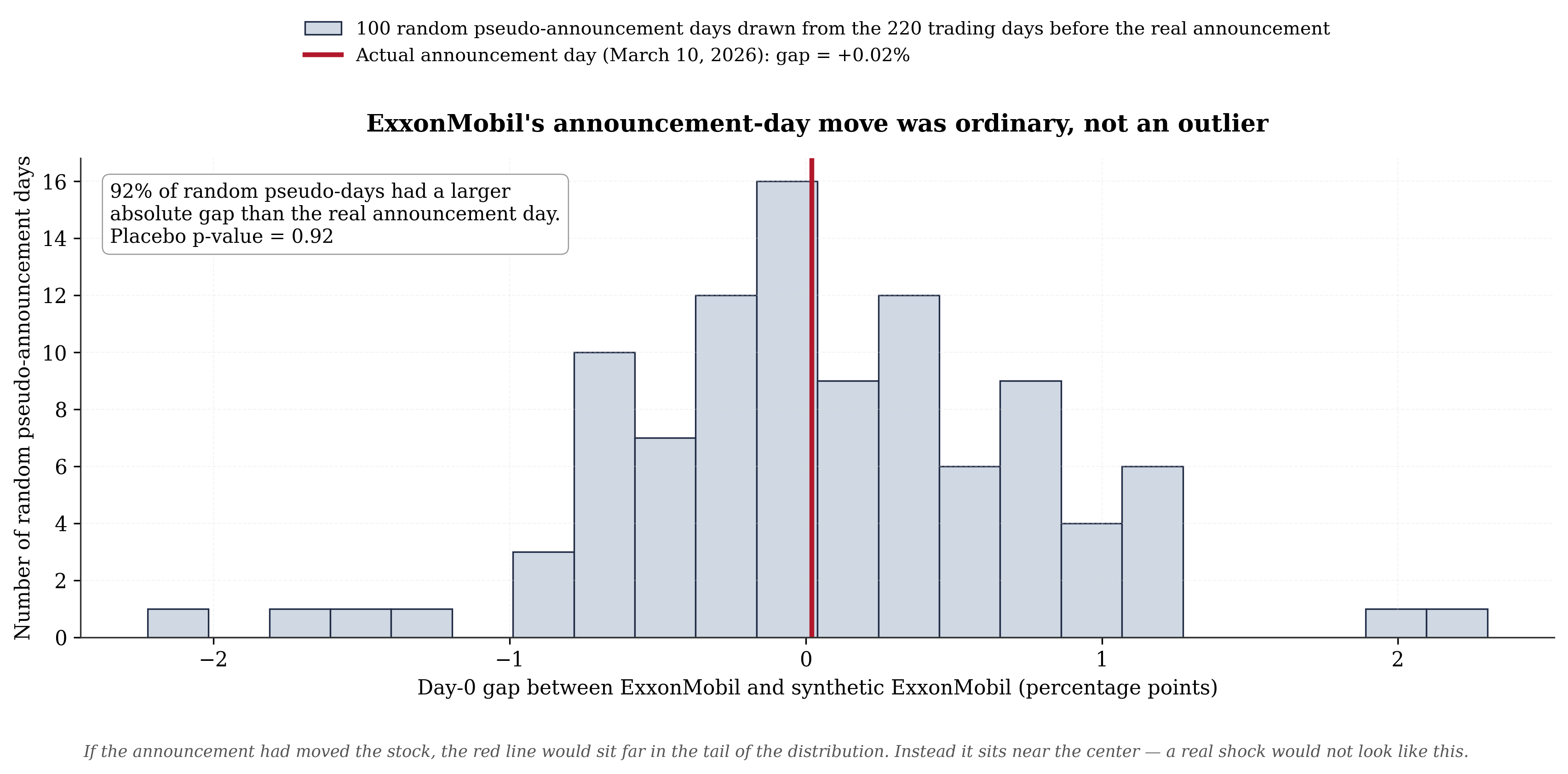

ExxonMobil's announcement-day move was ordinary, not an outlier

92% of random pseudo-days had a larger absolute gap than the real announcement day. Placebo p-value = 0.92. If the announcement had moved the stock, the red line would sit far in the tail of the distribution. Instead it sits near the center — a real shock would not look like this.

Method

In-time placebo: 100 random pseudo-announcement days drawn from the 220 trading days before the real announcement; same synthetic-control machinery applied to each.

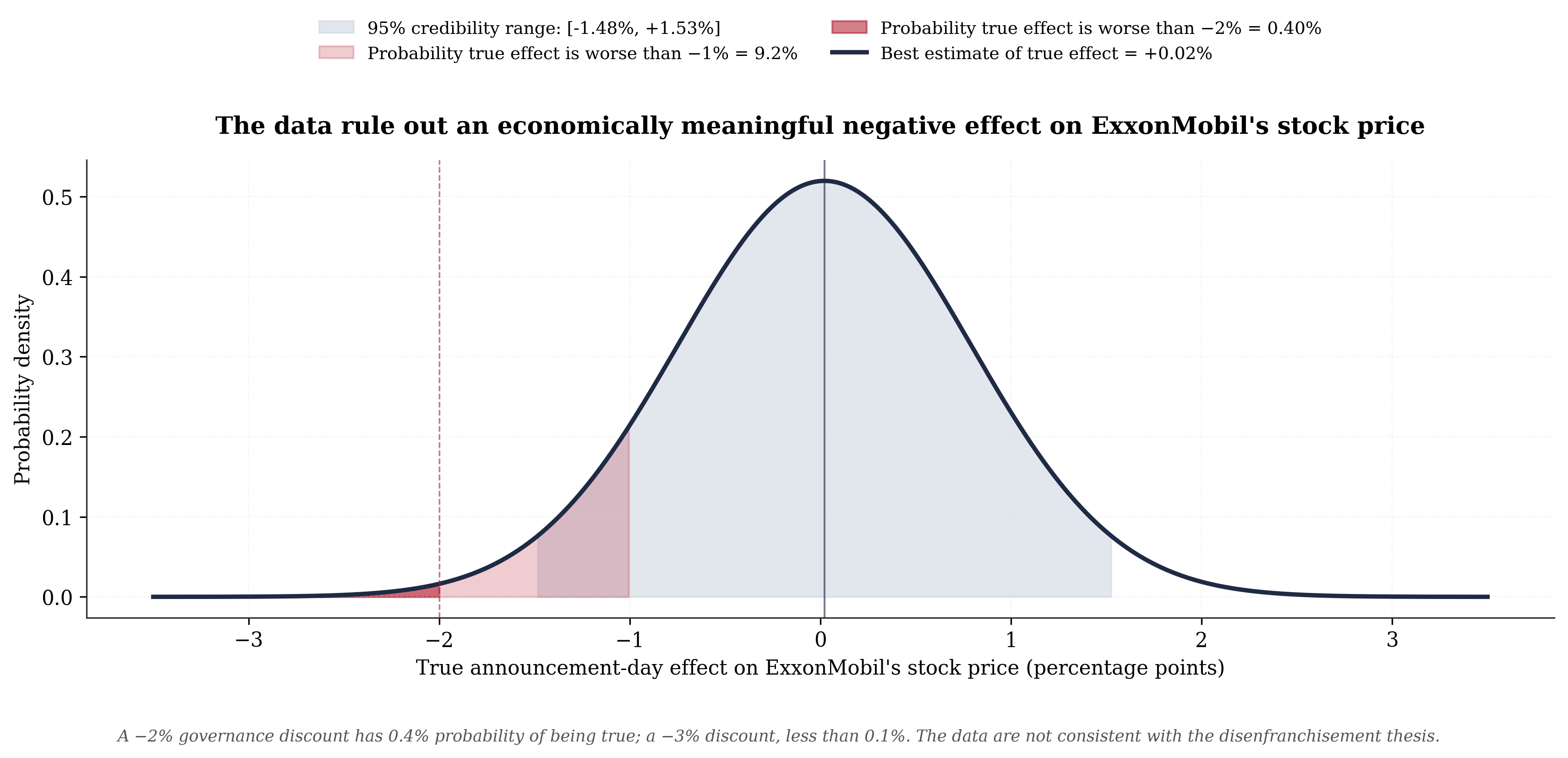

The data rule out an economically meaningful negative effect on ExxonMobil's stock price

Best estimate of true effect = +0.02%. 95% credibility range: [−1.48%, +1.53%]. A −2% governance discount has 0.40% probability of being true; a −3% discount, less than 0.1%. The data are not consistent with the disenfranchisement thesis.

Method

Bayesian posterior over the announcement-day true effect, weakly-informative prior, conditioned on the synthetic-control day-0 gap and pre-period RMSE.

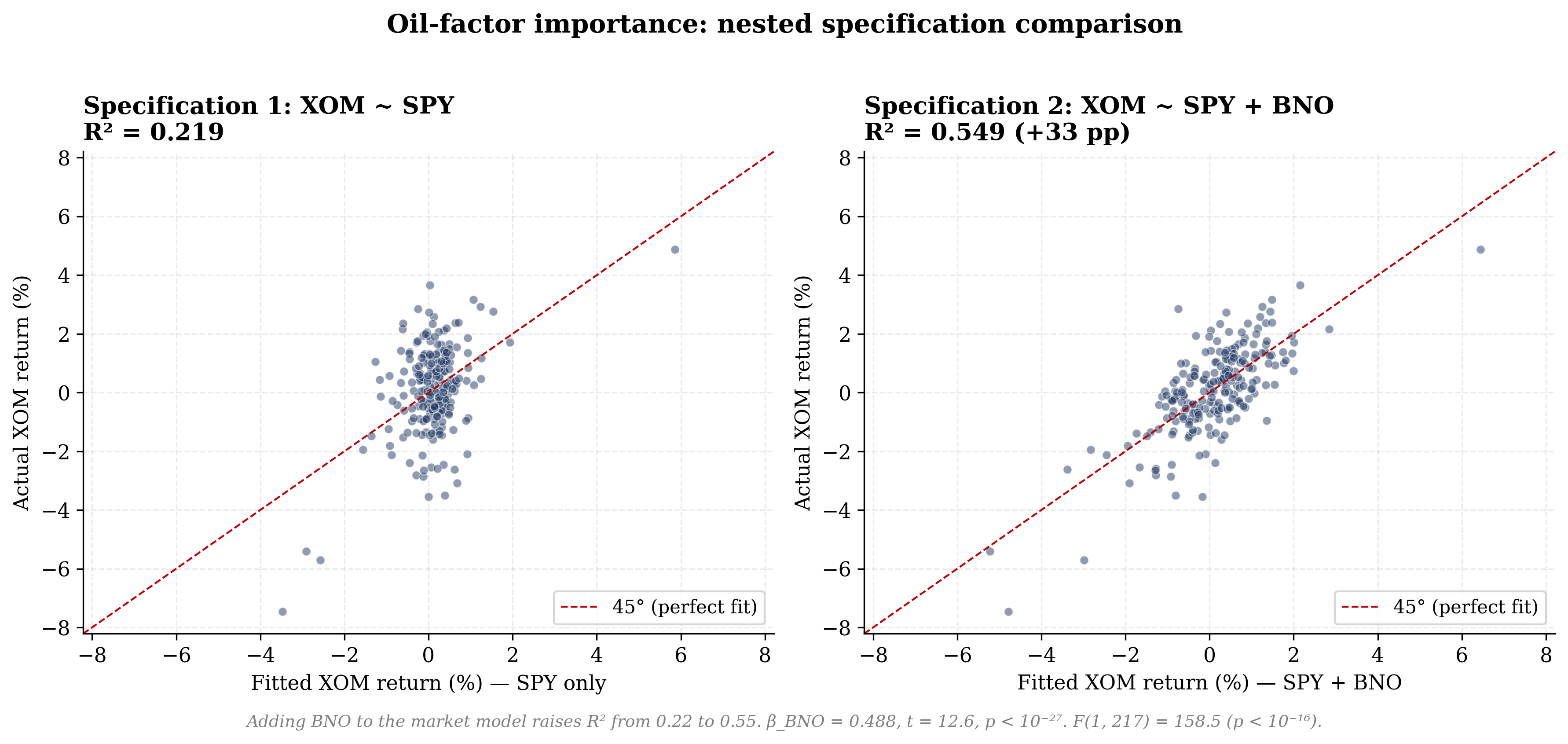

Adding BNO to the market model raises R² from 0.22 to 0.55. β_BNO = 0.488, t = 12.6, p < 10⁻²⁷. F(1, 217) = 158.5 (p < 10⁻¹⁶).

Method

Nested OLS comparison: Spec 1 = XOM ~ SPY (market only); Spec 2 = XOM ~ SPY + BNO (oil-augmented). Estimation window 2025-03-25 to 2026-03-09. Justifies oil-augmented as the preferred announcement-window benchmark.

Data integrity. Each PNG is byte-identical to the figure shipped with the FINAL_BLUE_SKY analysis package; SHA-256 verified at deploy time. The underlying coefficients trace to xom_rerun_results.json in the replication kit. Open methodology and underlying code →

Robustness checks — does the headline result hold up?

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

Pre-event drift check: the firm's daily abnormal return drifted by -0.0002% per day in the pre-event window (p = 0.820). no detectable pre-event drift ✓.— A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

Donor co-movement check:10 of 11 peer firms moved in the same direction as the treated firm on the event day (binomial p = 0.0117). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = 0.886 (good tracking); R² = 0.771 (fraction of pre-event variance explained); Durbin-Watson = 1.88 (no autocorrelation). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

Returns around the shareholder-vote (or written-consent) date.

Vote window CARs not yet computed (vote on 2026-05-27).

No long-run / pooled estimates available for this firm yet — run phase5z_compute_longrun.py on Windows to populate (requires effective date ≥ 3 months ago).

Cohort-level robustness battery

Heckman selection-corrected ATE · Romano-Wolf step-down + BH FDR · pooled BHAR. This firm's reading is shown in context of the full cohort.

This firm: raw p = 0.282, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

The Texas opt-in statutory regimes (TBOC §21.552 / SB 29 derivative threshold; TBOC §21.373 / SB 1057 shareholder-proposal threshold) are available only to firms that are nationally listed Texas corporations. ExxonMobil Corp. is not yet Texas-incorporated; the move is pending shareholder vote with a proposed effective date of 2026-05-27. These adoptions can be elected only on or after the firm's TX effective date.

Source filings

Primary-source documents on SEC EDGAR plus IR / search links.

EDGAR accession (canonical) — 0001193125-26-098908

Classification & audit trail

Bucket

D

Panel eligibility

PANEL_A_post_SB29

Audit status

TIER3_REVIEWED_REV61

Source confidence

VERIFIED_PROXY

Transaction status

PENDING

Audit notes

[rev61 2026-05-18] Tier-3 data-audit BLOCK landed: mechanism reclassified from 'Conversion' to merger / holding-company redomiciliation via plan of merger. DEF 14A 0001193125-26-147614 filed 2026-04-08; PRE 14A 0001193125-26-098908; record date 2026-04-01; board recommends FOR. Vote 2026-05-27. Post-vote: 8-K Item 5.07 (within 4 business days) + Certificate of Merger filings (NJ DORES + TX SOS) will close out the audit trail. R3 post-vote dispatch queued.

Related firms

Use these for cross-firm sanity checks — peers in size, sector, or destination.

Every numerical result on this page traces to one of the files below. A reviewer who runs the script in their language of choice and matches expected_results.json within the documented tolerances (±0.5 percentage points on point estimates, ±0.05 on p-values) has independently validated the methodology.

Data files

CSV

Daily prices

Every daily closing price for ExxonMobil, 21 energy-sector peer firms, the S&P 500, and Brent crude (BNO) over 713 trading days (June 2023 – April 2026). The only raw input the analysis needs.

A compact summary of the five event-study specifications. Each row is a method (synthetic control, market model, oil-augmented, matched pair, raw differential); each column is what that method says about the announcement-day reaction.

The complete machine-readable output of the published analysis: every point estimate, every p-value, every donor weight, every robustness diagnostic. What the firm page reads from.

Self-contained Python script that runs all five specifications from the daily prices file. About 200 lines; standard libraries only (pandas, numpy, scipy). Five minutes end-to-end.

R port of the Python script using quadprog for the synthetic-control simplex problem. Produces output_R.json in the same schema as the Python version for cross-platform verification.

The most comprehensive replication — includes the TOST equivalence test at ±2 percentage points and the full placebo permutation distribution that the Python and R versions skip. Requires synth, mat2txt, estout packages.

Pinned package versions for the Python replication. Use with pip install -r requirements.txt to recreate the exact environment the published numbers were computed in.

Preliminary proxy statement — the first public announcement of the proposed New Jersey-to-Texas reincorporation. Filed 2026-03-10. Accession 0001193125-26-098908.

Definitive proxy statement for the May 27, 2026 annual meeting. Contains the final reincorporation proposal text put to shareholders. Accession 0001193125-26-147614.

Rule 14a-12 soliciting material filed alongside the PRE 14A — additional communications to shareholders about the redomestication. Accession 0001193125-26-099413.

Headline to verify. Oil-augmented Day-0 AR = −2.19% (Patell p = 0.0488, significant at 5%) after controlling for energy-sector co-movement. If your replication produces a Day-0 AR within ±0.5 percentage points of −2.19% and a Patell p within ±0.05 of 0.0488, the methodology is validated. Otherwise, that is a real finding worth reporting.