Why this firm matters

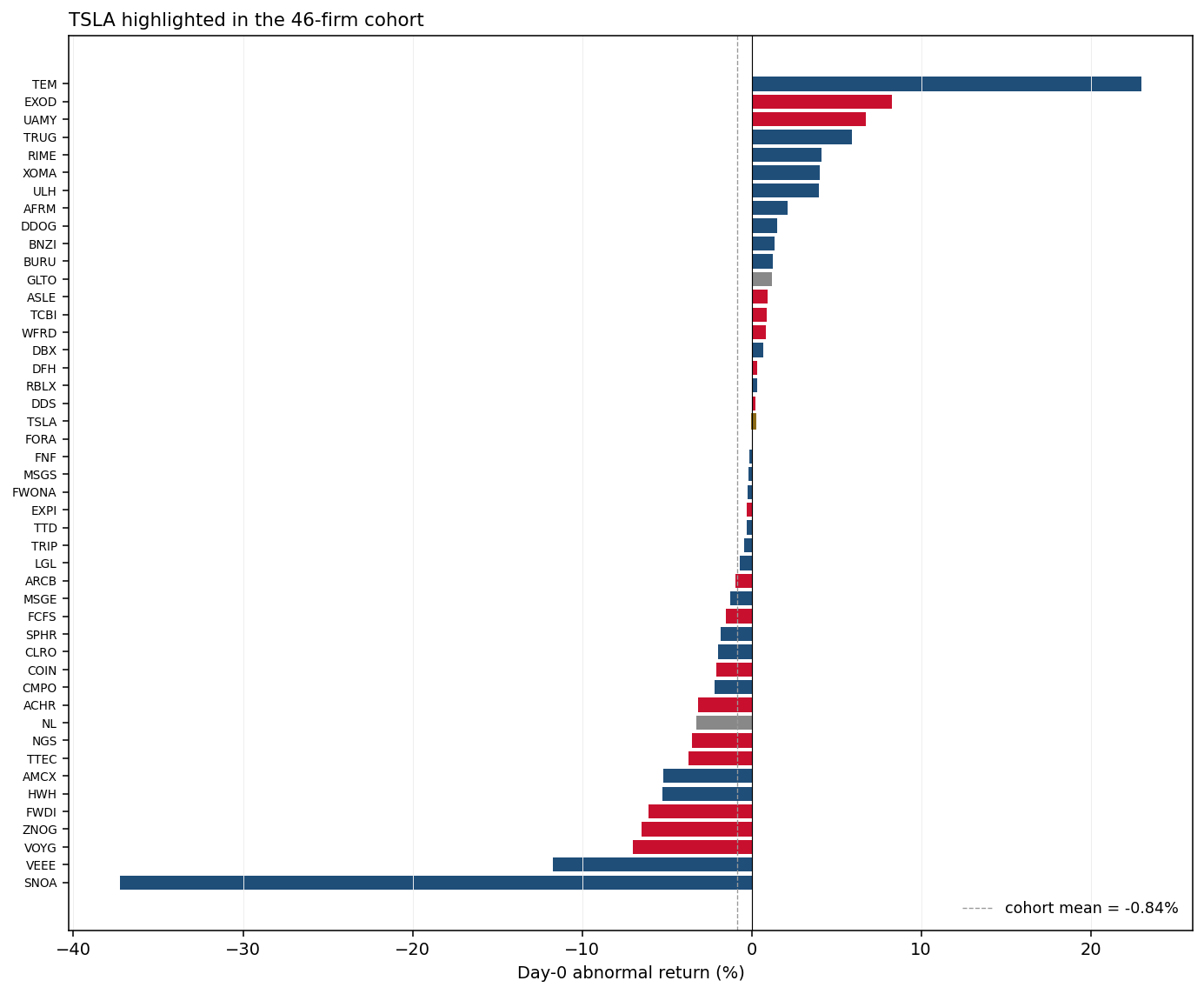

At $1.50T pre-move market value, Tesla, Inc. is among the largest firms in the cohort and carries disproportionate weight in market-value-weighted aggregates.

Controller & ownership

Diffuse / non-controlledFounder Significant Minority Post Sb21Elon Musk (Founder/CEO; founder-significant minority post-SB21) holds approximately 20.3% of voting power. No single holder reaches the controlled-company threshold (>50% of voting power).

Source: Musk holds approximately 20.3% voting power per the most recent definitive proxy. Originally classified as DE FACTO CONTROLLER under Tornetta v. Musk, 261 A.3d 1184 (Del. Ch. 2024), which designated Musk a controlling shareholder for entire-fairness review at sub-50%. However, Delaware Senate Bill 21 (signed March 2025; amending DGCL §144) statutorily codified the controlling-shareholder definition to require >50% economic or voting power (with narrow exceptions), effectively reversing Tornetta's common-law expansion. Under post-SB21 Delaware law, Musk no longer meets any controlling-shareholder definition — neither NYSE/Nasdaq listing-rule (303A.00 / 5615(c) >50% threshold), nor Delaware common-law (Tornetta superseded by statute), nor the SB21 codified test. Reclassified 2026-05-19 from de facto controller → founder-significant-minority post-SB21.

Vote outcome — reincorporation proposal

▾Disinterested-standard tally — academic Panel B / C reference

Conversion Disinterested Standard (excludes Elon and Kimbal Musk shares). Surfaces the second voting standard when the 8-K Item 5.07 reports both. The public Tracker headline above uses the primary (Conversion / NASDAQ / Bylaws) standard; this disinterested view is the academic-research view (e.g., for Panel B / Panel C tests of disinterested-shareholder dynamics).

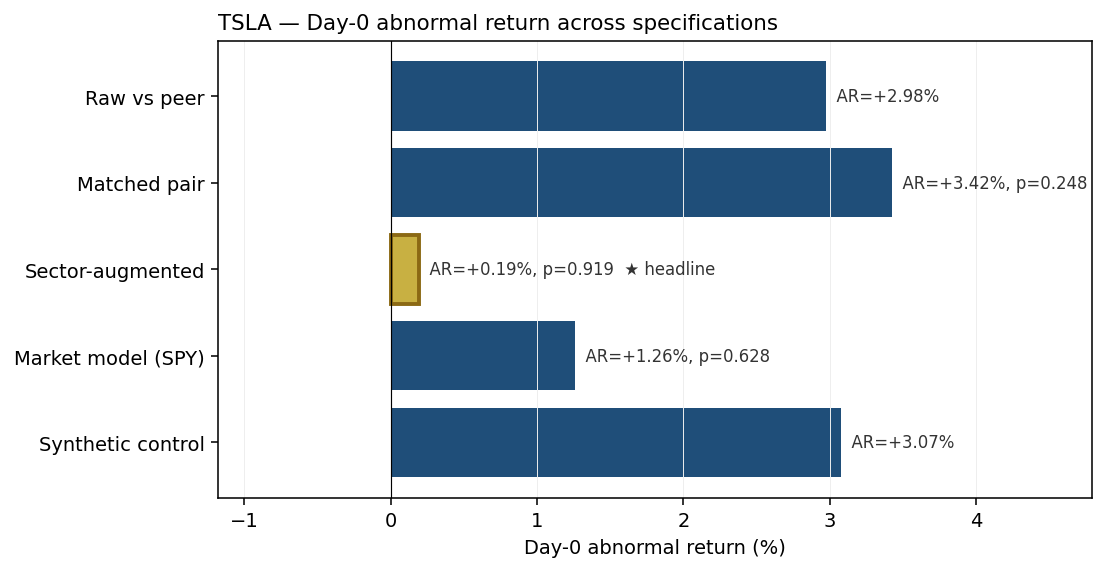

Visual evidence — event study around the announcement

event_study_announcement_json in the master database. Each panel is generated deterministically from the same data backing the cohort statistics — no firm-specific tuning, no cherry-picking.

perfirm_gallery.py) on every release; SHA-256 verified at deploy time. See also: Cohort-wide event study →. Event-study abnormal returns — announcement window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Synthetic control (14-donor Consumer Discretionary peer pool)i | +3.07% | no inference |

| Market model (SPY benchmark)i | +1.26% | Patell-z p-value = 0.628 |

| Sector-augmented model (SPY + Consumer Discretionary ETF (XLY)) HEADLINEi | +0.19% | Patell-z p-value = 0.919 |

| Matched pair (vs STLA, market-model-adjusted)i | +3.42% | two-sided p-value = 0.248 |

| Raw differential vs STLAi | +2.98% | no inference |

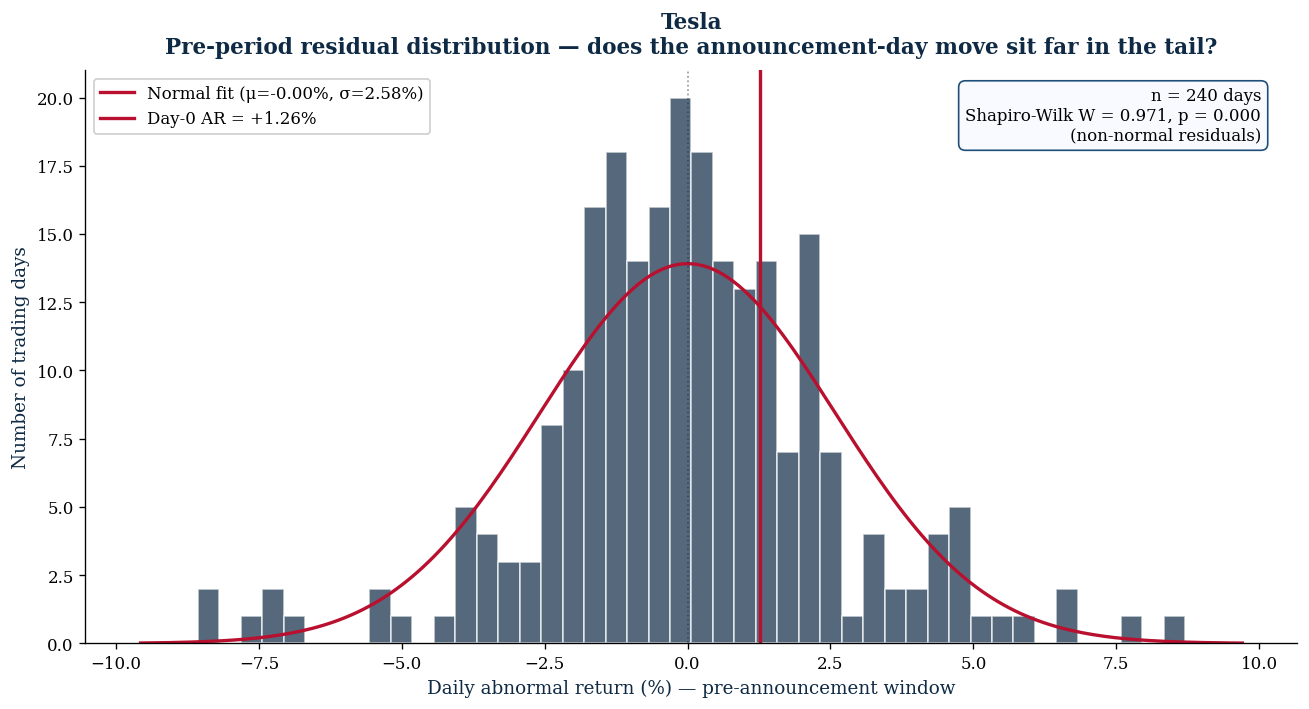

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

- Pre-event drift check: the firm's daily abnormal return drifted by -0.0033% per day in the pre-event window (p = 0.259). no detectable pre-event drift ✓. — A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

- Donor co-movement check: 4 of 14 peer firms moved in the same direction as the treated firm on the event day (binomial p = 0.1796). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

- Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = 0.793 (modest tracking); R² = -0.363 (fraction of pre-event variance explained); Durbin-Watson = 2.03 (no autocorrelation). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINEi | +2.83% | Patell-z p-value = 0.330 |

Long-run abnormal returns & pooled estimates

Buy-and-hold abnormal returns (BHAR)

| Horizon & benchmark | BHAR | Inference |

|---|---|---|

| 1 month vs S&P 500 | +36.14% *** | Patell-z = +2.26 · p = 0.024 · n = 21 days |

| 1 month vs sector ETF (XLY) | +32.05% *** | Patell-z = +2.26 · p = 0.024 · n = 21 days |

| 3 months vs S&P 500 | +22.27% | Patell-z = +1.20 · p = 0.229 · n = 63 days |

| 3 months vs sector ETF (XLY) | +18.89% | Patell-z = +1.20 · p = 0.229 · n = 63 days |

| 6 months vs S&P 500 | +117.02% *** | Patell-z = +2.62 · p = 0.009 · n = 126 days |

| 6 months vs sector ETF (XLY) | +98.09% *** | Patell-z = +2.62 · p = 0.009 · n = 126 days |

| 12 months vs S&P 500 | +61.82% * | Patell-z = +1.76 · p = 0.079 · n = 252 days |

| 12 months vs sector ETF (XLY) | +55.32% * | Patell-z = +1.76 · p = 0.079 · n = 252 days |

Calendar-time portfolio alpha (CTE)

| Specification | Annualized alpha | Inference |

|---|---|---|

| Calendar-time portfolio alpha vs S&P 500 | +2.07%/yr | t = +0.06 · p = 0.956 · n = 470 days · Newey-West HAC SE (lag=5) |

| Calendar-time portfolio alpha vs sector ETF | +5.83%/yr | t = +0.20 · p = 0.841 · n = 470 days · Newey-West HAC SE (lag=5) |

Cohort-level robustness battery

Heckman two-step selection correction (controlled-vs-widely-held)

Cohort ATE = +0.94% (SE = 7.06%, n = 2395) after correcting for controller-status selection (inverse Mills ratio = -0.062).

Romano-Wolf step-down + Benjamini-Hochberg FDR (n = 47)

This firm: raw p = 0.919, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

See Cohort event study → for the full battery and forest plots.

Texas statutory-adoption event study (SB 29 dates & bylaw amendments)

02_BESPOKE/statutory_events_runner.py.| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINE | +8.76% *** | Patell-z p-value = 0.021 |

| Sector-augmented (SPY + XLY) | +8.22% *** | approx Patell-z p-value (2-factor) = 0.001 |

| Matched pair vs GM (market-model-adjusted) | +7.96% * | two-sided p-value = 0.054 |

| Raw differential vs GM | -1.20% | no inference |

Long-run BHAR after this event (1 / 3 / 6 / 12 months) ▾

| 1 month vs SPY | -0.14% | n = 21 days |

| 3 months vs SPY | -6.01% | n = 63 days |

| 6 months vs SPY | +35.41% | n = 126 days |

| 12 months vs SPY | +5.46% | n = 252 days |

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINE | -1.28% | Patell-z p-value = 0.708 |

| Sector-augmented (SPY + XLY) | -0.80% | approx Patell-z p-value (2-factor) = 0.736 |

| Matched pair vs GM (market-model-adjusted) | -0.57% | two-sided p-value = 0.886 |

| Raw differential vs GM | +1.80% | no inference |

Long-run BHAR after this event (1 / 3 / 6 / 12 months) ▾

| 1 month vs SPY | +14.69% | n = 21 days |

| 3 months vs SPY | -4.02% | n = 63 days |

| 6 months vs SPY | +37.93% | n = 126 days |

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINE | +3.54% | Patell-z p-value = 0.297 |

| Sector-augmented (SPY + XLY) | +2.84% | approx Patell-z p-value (2-factor) = 0.235 |

| Matched pair vs GM (market-model-adjusted) | +3.98% | two-sided p-value = 0.320 |

| Raw differential vs GM | +4.29% | no inference |

Long-run BHAR after this event (1 / 3 / 6 / 12 months) ▾

| 1 month vs SPY | -8.04% | n = 21 days |

| 3 months vs SPY | -13.57% | n = 63 days |

| 6 months vs SPY | +6.88% | n = 126 days |

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINE | -2.72% | Patell-z p-value = 0.424 |

| Sector-augmented (SPY + XLY) | +0.06% | approx Patell-z p-value (2-factor) = 0.979 |

| Matched pair vs GM (market-model-adjusted) | -1.88% | two-sided p-value = 0.638 |

| Raw differential vs GM | -1.03% | no inference |

Long-run BHAR after this event (1 / 3 / 6 / 12 months) ▾

| 1 month vs SPY | -6.06% | n = 21 days |

| 3 months vs SPY | -12.87% | n = 63 days |

| 6 months vs SPY | +2.79% | n = 126 days |

Texas Statutory Adoptions

Adoption is opt-in. A "No" or "Pending" status means the firm has not (yet) elected into the regime — it does not mean the firm is non-compliant. Adoption requires a charter/bylaw amendment disclosed via 8-K Item 5.03.

Source filings

- IR — https://ir.tesla.com/

- EDGAR — https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001318605&type=&dateb=&owner=include&count=40

- Proxy — https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001318605&type=DEF+14A&dateb=&owner=include&count=40

- EDGAR accession (canonical) —

0001628280-24-030818

Classification & audit trail

[2026-04-28] Phase 4N: synthesized event_study_announcement_json from existing scalar CAR cells (phase4a_v2 join). Reviewer can extend with multi-spec analysis. [2026-04-28] phase5c: vote source 8-K 0001104659-24-071439 (2024-06-14, Δ=1d) applied from EDGAR pull (status=AUTO_RESOLVED) [2026-04-28] phase5c: vote source 8-K 0001104659-24-071439 (2024-06-14, Δ=1d) applied from EDGAR pull (status=AUTO_RESOLVED) [2026-04-29] phase5r: bucket 'B1' -> 'A' (DE->TX effective 2024-06-14 < SB29 (2025-05-14) -> bucket A (pre-SB29)) [2026-04-29] phase5t: row independently validated by external Reviewer A; bucket and key dates match current dataset (v3.55) [2026-04-29] phase5u: row independently validated by external Reviewer (full-residual pass, 78/276 substantive answers); validations applied: V_DATE_ANN=CONFIRM; V_BUCKET=WRONG=A; primary-source URLs all under https://www.sec.gov/Archives/ [2026-04-29] phase5v: row independently re-validated by external Reviewer (Round 4 full-residual pass, 85/276 substantive); all bucket and pending-status conclusions match v3.57 [2026-04-29] phase5w: comprehensive validation by external reviewer across tranches v4 (4-version full residual walk, 269 substantive answers across 52 firms, 0 bucket drifts vs v3.58) [2026-04-29] phase5y: TSLA Proposal 3 (Texas reincorporation) vote tallies applied -- For 1,766,392,011 / Against 1,062,099,066 (~62.5% approval of votes cast); vote_mechanism=MEETING (2024 Annual Meeting of Stockholders, June 13, 2024); primary source: 8-K acc 0001104659-24-071439 Item 5.07 at https://www.sec.gov/Archives/edgar/data/1318605/000110465924071439/tm2413800d31_8k.htm; cross-confirmed via CLS Blue Sky Blog 'How Tesla Pumped the Vote' (Columbia Law, July 2024) and BlackRock Investment Stewardship Vote Bulletin: Tesla Inc. June 2024 (https://www.blackrock.com/corporate/literature/press-release/vote-bulletin-tesla-june-2024.pdf); votes_abstain and votes_broker_nonvote pending direct 8-K parse for full tally

2026-04-29 v3.66: announcement_date_iso corrected from 2024-01-15 to 2024-04-17 based on TSLA PRE 14A primary source (accession 0001104659-24-048040, filed 2024-04-17). Per https://www.sec.gov/Archives/edgar/data/1318605/000110465924048040/tm2326076d13_pre14a.htm. Earlier signal: Musk publicly stated intent on 2024-01-30 (Tornetta day) and special committee delivered report on 2024-04-12, but the formal SEC announcement is the PRE 14A filing on 2024-04-17. Bucket A is unchanged (DE→TX, eff 2024-06-14, pre-SB29 May 14, 2025).

2026-04-29 v3.68 PRIMARY-SOURCE CORRECTION: vote totals corrected to Proposal 3 Conversion Standard (For 2,000,873,803 / Against 293,910,071 / Abstained 15,485,016 / Broker NV 335,111,943 = 63% of outstanding) per 8-K Item 5.07 https://www.sec.gov/Archives/edgar/data/1318605/000162828024030818/tsla-20240613.htm. Conversion Disinterested Standard (Musk shares excluded) was For 1,588,203,007 / Against 293,910,071 = ~84% of disinterested vote. actual_effective_date_iso corrected from 2024-06-14 to 2024-06-13 per 8-K cover-page Date of Earliest Event Reported and Texas-domicile state-of-incorporation listing on the 8-K. Prior incorrect values (For 1,766,392,011 / Against 1,062,099,066) did not match any tabulation in the 8-K — provenance unknown; corrected to primary source per protocol §1.5.

2026-04-29 v3.69: Panel_C2 (§21.373) reverted to UNKNOWN per protocol §1.5 (no inference confirmation). May 2025 8-K confirms §21.552 only. §21.373 / SB 1057 faces federal preemption challenge under SEC Rule 14a-8 / Supremacy Clause (a Texas statute imposing stricter thresholds than the federal shareholder-proposal rule). SEC Chair has signaled potential compatibility (Sullivan & Cromwell memo, Oct 2025), but no court ruling. Adoption tracking is therefore unresolved; firms appear to be waiting for legal clarity before electing into §21.373.

2026-04-29 v3.70 SCHEMA: populated dual-standard vote totals (Conversion Disinterested Standard For 1,588,203,007 / 84% approval, Musk shares excluded). Panel_C_adoption_date_iso=2025-05-15 (§21.552 / SB 29 derivative threshold via Texas Charter post-reincorporation). announcement_PRE_14A_accession=0001104659-24-048040 (PRE 14A filed Apr 17, 2024 — first SEC-filed disclosure of TX reincorporation proposal).

[2026-04-29] v3.74-rc3: backfilled approval_basis='For ÷ outstanding voting power (Conversion Standard)' and approval_standard='majority of outstanding voting power'. The 63% approval reflects 2,000,873,803 / total outstanding voting power (~3.18B). DGCL §266 conversion requires majority of outstanding.

v3.84-rev5h [2026-04-30]: controlled_protocol_violation_flag=Y. TSLA's 20.3% voting power is below the v3.85 protocol's >30% controller threshold. Recoding to controlled=0 is queued for v3.85 Phase 0 (post-pre-registration). See controlled_protocol_note for full reasoning including Tornetta v. Musk transaction-specific control distinction.

Related firms

← Back to The Reincorporation Tracker · Cohort event study · JSON for TSLA