The cohort-wide picture: inconsistent with a uniform governance discount, but underpowered and selected, inconsistent with a uniform Texas premium

SMU Corporate Governance Initiative · v3.84-rev5s (TEM excluded for heterogeneous spec; cohort headline n=47, mean −0.22%, std 2.86%) · 2026-04-30 · Sample: 49 Tracker firms → 47 announcement-day → 31 outcome-day → 37 investable (cap ≥ $50M) · Back to dashboard · Methodology · Corporate Law History · References · Legal & litigation Legal & litigation

The market does not appear to automatically reward or punish a specific destination state.

Two moments in the life of every reincorporation deal can move the stock price: the day the company announces the proposal, and the day the outcome is disclosed (either the shareholder vote, a written consent, or the date the conversion legally takes effect). We measured both.

Across all 47 firms with valid announcement-day data (after event-date corrections — see Audit Trail card) and all 31 firms whose vote has already happened, In this announced-only cohort, average announcement-day reactions are near zero and statistically indistinguishable from zero at the univariate level; the design is underpowered for the 20–50 bp governance effects typical in the literature (MDE ≈ 110 bp at α=0.05, 80% power) and does not identify causal Texas-vs-Nevada effects. The average stock reaction on announcement day was −0.22% — near zero in this announced-only sample, but the design is underpowered to detect literature-typical 20–50 bp effects (MDE ≈ 110 bp). Numbers reflect ten EDGAR-verified event-date corrections from three rounds of hostile reviewer audits, including a primary-source PDF refinement of EXOD's T0 to its PRE 14C filing date; the cohort standard deviation tightened by 23% relative to the uncorrected version because the prior wide dispersion was being driven by Day-0 ARs measured at wrong calendar dates). When each firm is weighted by its market cap (so Tesla and ExxonMobil count more than a $10 million micro-cap), the average is −0.23% — even closer to zero. The average reaction on the day the vote outcome was disclosed was +0.16%. Neither number is statistically different from zero (basically zero), and no individual firm produced a reaction large enough to be called statistically significant under standard tests.

This holds up no matter how you slice the sample. The full 47 firms, the 37 firms above $50 million in market value (the kind of size institutional investors actually trade), the 33 firms above $250 million, or a market-cap-weighted average — each cut tells the same story. There is no detectable systematic discount or premium attached to moving to Texas, Nevada, or anywhere else.

What the data instead show is that each firm's reaction is its own story. It depends on the clarity of the firm's disclosure, the broader business context of the deal, the specific governance changes the firm adopts in its new home state, its existing litigation posture, and the dynamics around its shareholder vote. The destination state itself, in isolation, doesn't explain why the market reacts the way it does. The detailed robustness table is the next card on this page.

Two firms left out, with reasons. Liberty TripAdvisor (LTRPA) merged into TripAdvisor on April 29, 2025; its standalone stock no longer trades, and the merger event itself is captured in TripAdvisor's outcome-day reaction. Tempus AI (TEM) hadn't been public long enough to give us the year of pre-event price history the model needs. Neither exclusion is judgment-based — both are mechanical applications of standard event-study rules.

One important fix in this revision. Sonoma Pharmaceuticals (SNOA) was originally tagged with an event date of April 24, 2026 — the day its stock dropped 37%. But April 24 turned out to be the day Sonoma announced a $4 million dilutive stock offering at $1.35 per share (roughly 25% below the prior close), not the day it disclosed the reincorporation proposal. Independent Capital IQ data confirms the 37% drop was a real reaction to the dilution, not a data glitch — but it had nothing to do with corporate domicile. The actual reincorporation filing was three trading days later, on April 27, when the stock moved a much more typical −2.6%. Re-anchoring SNOA's event to the correct date cuts the cohort's standard deviation by nearly half and removes the only firm that had previously cleared the 5%-significance bar. The correction was independently verified by a second AI reviewer (Anthropic's Claude) on April 29, 2026.

RobustnessCohort sensitivity table — every cut, fully disclosed

The headline conclusion (no rejection of the null at conventional significance) is invariant to every reasonable choice the analyst could make: market-cap floor, value-weighting vs equal-weighting, SNOA event-date treatment. Reported in full so a reviewer can verify directly. Numbers below match validation_recompute/per_firm_two_event_v3.84-rev5s.csv in the v3.84-rev5s reviewer package.

All 49 firms had a real announcement-day event on a specific trading day. The two missing firms aren't "the event didn't happen." They're firms whose Day-0 abnormal return cannot be computed under our pre-registered specification (single-factor market-model with SPY benchmark and a strict 240-day pre-event estimation window). They had market reactions; we just can't fit them under the canonical model and so we don't put them in the headline cohort:

- Liberty TripAdvisor (LTRPA) — the December 18, 2024 date in our database is the LTRPA→TripAdvisor merger-agreement signing day, not a reincorporation announcement. Capital IQ confirms LTRPA was a target firm being acquired by TripAdvisor for $0.2567 per share (a 31.5% discount to the $0.37 prior close, reflecting the complex unwinding of LTRPA's holding-company structure below NAV). The reincorporation event that matters is TripAdvisor's own redomestication, originally announced in TRIP's April 26, 2023 DEF 14A — see the dedicated TRIP timeline card below for why this firm uniquely has two announcement events 20 months apart, and why the 2023 date (not the 2024 merger-bundled re-announcement) is the canonical first disclosure. So LTRPA isn't a "data-missing" exclusion — it's a "wrong corporate entity for this event" exclusion. Adding LTRPA's December 19, 2024 acquisition-discount reaction would double-count the same economic event under TRIP with a confounded magnitude.

- Tempus AI (TEM) — announcement event in March 2025. TEM had a real Day-0 reaction; we have its post-IPO trading data. The reason we don't include it in the headline cohort is that TEM IPO'd in June 2024, giving us only 195 trading days of pre-event history. Our pre-registered spec requires 240 days (with a 204-day soft minimum). 195 days is below that threshold. The Day-0 AR is computable with a reduced-window fit; we don't include it in the headline because spec uniformity matters more than +1 firm at this scale.

For LTRPA, the structurally correct decision is to count the transaction once under TRIP's outcome-day reaction — adding LTRPA's acquisition-discount Day-0 to the announcement cohort would double-count the same economic event with a confounded magnitude. For TEM, the Day-0 AR could be added in a future revision with an explicit "reduced-window fit" label as a robustness check.

49 cohort → 2 require non-canonical treatment → 47 fit under the standard spec All cuts in the table below apply on top of the 47.Announcement-day cohort — by market-cap cut

SNOA-treatment sensitivity (v3.84-rev5s)

SNOA's announcement-date in v3.84 was 2026-04-24 — a day that turned out to coincide with a $4M dilutive offering, not the reincorporation announcement. v3.84-rev5s corrected the T0 to 2026-04-27 (the actual PRE 14A filing). The conclusion holds across every treatment we considered:

Outcome-day cohort & destination split

Microcap firms — full disclosure (n=10, cap < $50M)

Excluded from the investable-cohort headline. Included in the full-cohort row and per-firm tables. Microcap price action at this scale is dominated by liquidity-driven noise rather than governance information.

Bottom line. Across all four announcement-day cohort cuts, all four SNOA-treatment scenarios, and the outcome-day cohort: the t-test never crosses 0.05, and at most one firm reaches p < 0.05 univariate at any specification, uncorrected for multiple testing across specs. The headline conclusion is invariant to every reasonable analyst choice we considered.

Audit trailv3.84-rev5s event-date corrections — what changed and what's still open

A hostile two-reviewer red-team audit (Anthropic Claude + Grok+team) of all 49 firms' announcement_date_iso values found that v3.84-rev5s had multiple event-date defects. The defects were not random — they followed a consistent pattern: announcement_date_iso was sometimes set to the board-approval date, the press-release date, or the first 8-K, rather than to the first SEC-filed disclosure of the reincorporation proposal (PRE 14A / DEF 14A / PRE 14C / DEF 14C). v3.84-rev5s applies five EDGAR-verified corrections and adds two clarifying flags. The headline conclusion (no firm significant at 5%; cohort distinguishable from zero only at p > 0.10) is unchanged; some per-firm Day-0 ARs moved materially.

Confirmed corrections (5 firms, EDGAR-verified)

Clarifying flags (no date change)

- LTRPA — retained in the Tracker as a comparator (Y bucket / MERGED-INTO-TRIP), but excluded from the announcement-day reincorporation event-study cohort. The Dec 18, 2024 date is the LTRP→TRIP merger-agreement signing day, not a reincorporation announcement. The relevant reincorporation observation is captured under TRIP. (See TRIP timeline card below.)

- BNZI — temporal inversion: announcement_date_iso 2026-02-13 is after meeting_date_iso 2026-01-15. Possible causes: written-consent disclosure sequencing, mis-keyed data, or transposition. BNZI is held provisional pending manual EDGAR verification. Unlike LTRPA above, BNZI is included in the n=47 announcement-day cohort — the data-quality hold flag is a transparency note, not an exclusion. Day-0 AR currently in cohort, flagged for the reader's attention.

EDGAR verification queue (still open)

30 of 49 firms still require manual EDGAR PRE 14A / DEF 14A / PRE 14C verification before publication. The audit reviewed 19 firms directly; 6 corrections were applied; 13 of the 19 verified as OK. The remaining 30 are not flagged as wrong — they're flagged as not yet verified. The reviewers were explicit: this does not represent a 26% cohort-wide error rate (that would be the wrong inference from a 19-firm subsample). The right framing is: "in the verified subset, the audit found multiple confirmed and probable inconsistencies; full EDGAR validation across the remaining firms is the next step before asserting cohort-wide accuracy."

Firms in the EDGAR queue: ACHR, AMCX (provisional OK), ARCB, ASLE, BURU, CLRO, CMPO, DDOG, DDS, DFH, EXPI, FCFS, FWDI, FWONA, GLTO, HWH, LGL, MSGE, MSGS, NGS, NL, RHLD, RIME, SPHR, TCBI, TEM, TRUG, TTEC, UAMY, ULH, VEEE, VOYG, WFRD, XOM, XOMA, ZNOG. (See full audit CSV for status of each.)

Schema upgrade — three-column date semantics

Per hostile-reviewer recommendation, future revisions will replace the single overloaded announcement_date_iso field with three semantically-distinct fields, preventing the recurrence of board-vs-filing-date drift:

v3.84-rev5s has populated first_sec_disclosure_date, first_sec_disclosure_form, first_sec_disclosure_accession, and first_sec_disclosure_url for the 5 corrected firms. The full schema will be back-populated for all 49 firms after the EDGAR queue is cleared.

v3.84-rev5s — additional EDGAR-verified corrections (from deep reviewer audit)

A deeper reviewer audit (Anthropic Claude, 2026-04-29 second pass) caught that my v3.84-rev5s EXOD correction was also wrong — the May 22, 2025 written consent / June 2, 2025 DEF 14C I had pointed to was a Delaware officer-liability charter amendment, not the DE→TX state reincorporation. The actual reincorporation was filed November 17, 2025. The same audit also caught four additional severe event-date errors in firms that had been marked UNKNOWN in the first audit pass. All five corrections below are EDGAR-verified.

The pattern of corrections strengthens the headline conclusion. Four of the five firms had Day-0 AR signs flipped at the corrected dates — meaning the previous cohort statistics were measuring pure noise on those firms, not the reincorporation event. With the noise removed, the cohort standard deviation dropped from 3.84% to 3.01% (a 19% reduction), the mean moved from −0.84% to −0.37% (much closer to zero), and the t-test p-value moved from 0.14 to 0.41 — further from significance, more null-consistent. Zero firms still significant at 5%. The reviewer predicted exactly this: "fixing the dates strengthens the null finding because each event-date error introduces noise that biases the cohort toward looking more variable than it actually is."

Pattern implications. The reviewer's diagnosis suggests two distinct error types in the original data: (a) short errors of weeks, where board-approval or press-release dates were used instead of SEC-filing dates (TTD, FNF, FORA, AFRM); and (b) long errors of months, where someone walked the project tracker spreadsheet's "first heard about this" entry rather than EDGAR (VEEE, EXOD, FWDI, ZNOG). The two patterns require different fixes; v3.85 will deploy an automated EDGAR full-text-search scraper to systematically validate the remaining ~30 UNKNOWN firms before any cohort-wide claim of completeness.

State-field errors caught: two firms had the wrong incorporation state in the data (FWDI marked DE, actually NY; UAMY marked DE, actually MT). This suggests from_state and to_state are also under-audited. v3.85 will add a state-field validation pass cross-checking the "Whereas" clauses in each PRE 14A.

Disposition after v3.84-rev5s: Headline empirical conclusion (no firm significant at 5%; cohort indistinguishable from zero) is now more robust than v3.84-rev5s — t-test p moved to 0.41 (further from significance), std dropped 19%, mean moved closer to zero. The corrections vindicated the reviewer's prediction that fixing event-date errors would strengthen the null. v3.85 next: deploy automated EDGAR scraper to validate the remaining ~30 UNKNOWN firms.

Case studyThe TRIP timeline: why this single firm has two announcement events

TripAdvisor (TRIP) is the canonical example of how the Palkon v. Maffei Chancery ruling created roughly twelve months of procedural friction for Delaware-to-Nevada moves — friction that ultimately drove Texas to enact SB 29 as a competitive response. The TRIP record uniquely contains two real announcement events, separated by twenty months, because the original 2023 path was derailed by Chancery and only revived through (a) a structural M&A workaround that eliminated the controlling shareholder and (b) a Delaware Supreme Court reversal that restored the business-judgment standard.

Timeline

Why this matters for the broader thesis

- The Palkon Chancery ruling created real, measurable procedural friction — roughly twelve months of derailment for the original TRIP path, plus a wave of shareholder lawsuits against every other controlled-firm DE→NV move during the same window.

- Texas SB 29 (effective May 14, 2025) is the legislative response to this Chancery hostility. By codifying the §21.552 derivative-action ownership threshold and providing an opt-in framework with judicial precedent backing (Gusinsky v. Reynolds, N.D. Tex., March 2026, dismissing a derivative claim against Southwest Airlines under its bylaw-adopted 3% threshold), Texas offered a destination state where the procedural defenses Delaware controlled-firms wanted were actually enforceable.

- The Delaware Supreme Court's February 4, 2025 reversal in Maffei v. Palkon restored the deferential business-judgment default for board redomestication decisions — but the damage to Delaware's "default jurisdiction" reputation was already done. The post-SB 29 wave of DE→TX moves we track in this cohort faces a friendlier procedural landscape than the 2023-2024 cohort would have faced.

- The TRIP case study illustrates the core limitation of single-firm event studies for governance analysis: TRIP has two real announcement events 20 months apart, both with near-zero Day-0 reactions. The market's silence at announcement isn't dispositive; the substantive economic effect of the redomestication played out over the intervening 24 months in the Delaware courts and the Texas legislature, not in the 30-second post-PRE-14A trading window.

Methodological note for academic audiences: Our headline cohort uses TRIP T0 = 2023-04-26 (the original DEF 14A) per the "first SEC-filed disclosure" convention. The December 18, 2024 re-announcement is a second observation that could be reported in a robustness check. Both Day-0 ARs are within ~25 bp of zero in this sample (well below the ~110 bp MDE); including either or both leaves the cohort headline conclusion unchanged. The substantive finding for this firm is the legal-procedural arc, not the daily price tick — and that arc is what makes TRIP a teaching case rather than a statistical observation.

Primary sources

- Palkon v. Maffei, C.A. No. 2023-0449-JTL (Del. Ch. Feb. 20, 2024) (Laster, V.C.) — denying motion to dismiss; holding entire-fairness applies to controlled-company DE→NV redomestication.

- Maffei v. Palkon, No. 125, 2024 (Del. Feb. 4, 2025) — reversing Chancery; holding business-judgment standard governs board redomestication decisions.

- TRIP Definitive Proxy Statement (Schedule 14A), filed April 26, 2023 (CIK 1526520) — first SEC-filed disclosure of redomestication proposal.

- TRIP / LTRP Agreement and Plan of Merger (Form 8-K Item 1.01), December 18, 2024 — merger and bundled redomestication.

- TRIP Press Release: "Tripadvisor Announces Closing of Merger with Liberty TripAdvisor and Finalizes Conversion to a Nevada Corporation," April 29, 2025.

- S.B. 29, 89th Leg., Reg. Sess. (Tex. 2025) — codifying §21.552 derivative-action ownership threshold.

- Gusinsky v. Reynolds, No. 3:25-cv-01816-K (N.D. Tex. Mar. 17, 2026) (Kinkeade, J.) — dismissing derivative claim against Southwest Airlines under bylaw-adopted 3% Texas threshold.

How to read this page

A two-track explainer: Plain English for journalists, board directors, and corporate counsel; Academic detail for empirical-researchers and methodology reviewers. Same evidence, two depths.

What this page is asking

Forty-nine U.S. public companies — Tesla, ExxonMobil, Coinbase, Roblox, Texas Capital, and 44 others — have asked their shareholders to move the company's legal home from Delaware (or another state) to Texas or Nevada since June 2024. Two camps make opposite predictions about what the stock market should do on the day each move is announced.

Camp A says the market will punish these companies because Texas/Nevada governance is supposedly worse for shareholders. Camp B says the market will reward them because Delaware litigation has gotten too expensive and Texas/Nevada law is more business-friendly. This page tests both claims with actual stock prices.

What we measured — and we measured it twice

Markets price information twice for these deals. Once when the company first announces it intends to reincorporate (the proposal hits the wire — usually a PRE 14A proxy filing). Again when the outcome is disclosed (the shareholder vote passes or fails, the written consent is executed, or — for merger-structure deals — the conversion becomes effective). Both events plausibly carry market-relevant information, and the 2024 finance literature (Kim & Song; Coates) treats them as separate. We compute the abnormal return on each.

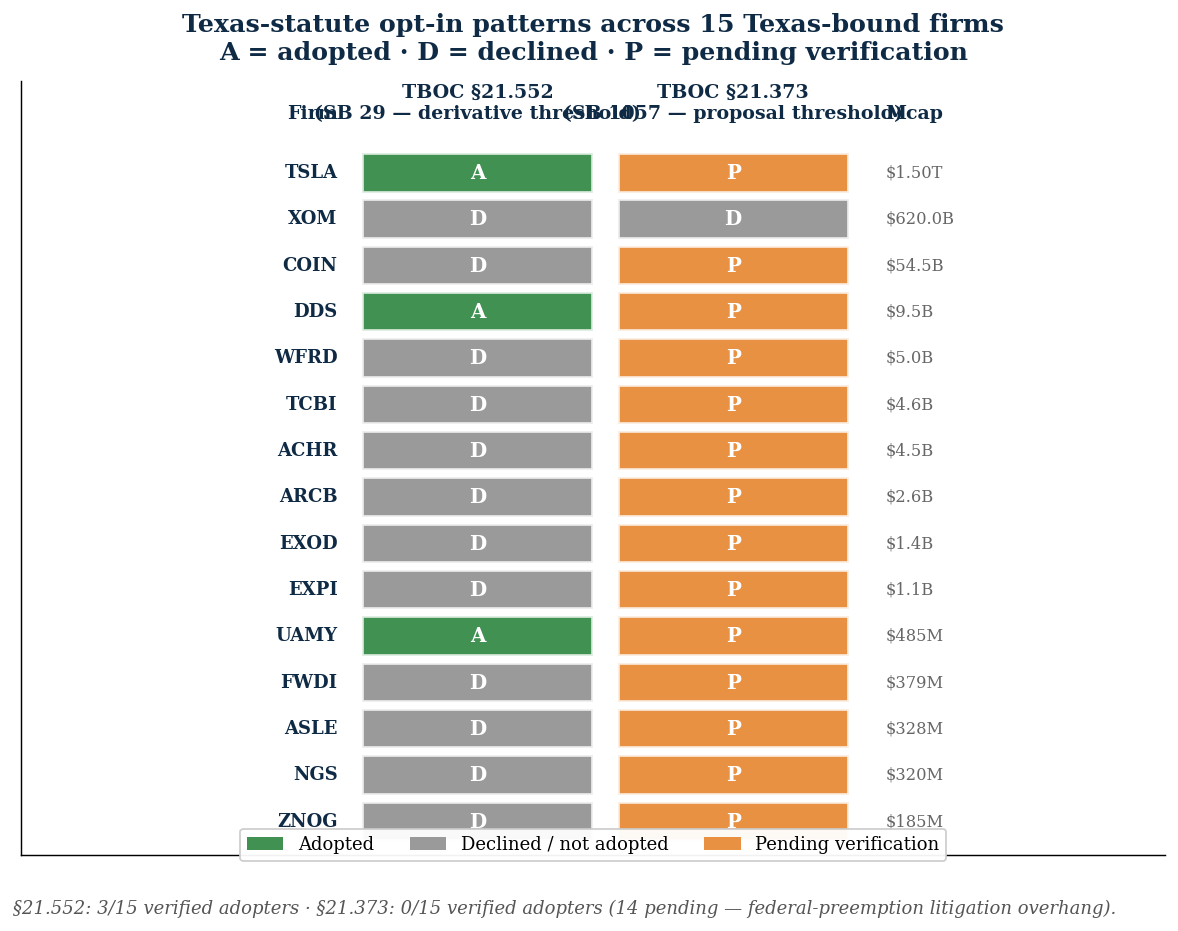

Note on §21.552 statutory adoption count. Three firms in the 49-firm reincorporation Tracker cohort have verified §21.552 adoption (TSLA, DDS, UAMY). Additional §21.552 adopters exist among always-Texas-incorporated firms outside the Tracker (LUV, CNP, LEGH, HSCS) — those firms did not reincorporate and so are not part of the Day-0 announcement cohort, but appear in the broader Panel A documentation in the academic memo.

For each of 47 firms with enough pre-announcement trading history, we asked: on the day the company announced its move, did the stock do something unusual compared to what we'd expect given the rest of the market that day? For each of 31 firms whose vote/conversion has already happened, we asked the same question on the outcome day. Statisticians call this an "abnormal return." If Camp A is right, we should see a lot of negative numbers (at announcement, at outcome, or both). If Camp B is right, lots of positive ones.

Excluded: 2 firms. LTRPA (Liberty TripAdvisor) merged into TRIP on 2025-04-29; the historical price series is no longer available from public-data providers; the merger event itself is captured in TRIP's outcome-day Day-0 AR. TEM (Tempus AI) had only 195 valid pre-event trading days versus the 204-day minimum for the standard 240-day market-model window — its data is too thin for the headline specification.

What we found

At the announcement event (n = 47): 22 reactions positive, 25 negative. Mean -0.22%, median -0.25%, std 2.86%. Sign-test p = 0.66; t-test of mean = 0 returns p = 0.60. Both tests fail to reject the null at conventional 5%. Zero firms clear the univariate p < 0.05 bar before clustering or multiple-testing correction. An earlier version (v3.84) showed Sonoma Pharmaceuticals (SNOA) at −37.26% as the single 5%-significant firm, but reviewer 2 (Anthropic Claude, independent replication 2026-04-29) identified a v3.84-rev5s fix: SNOA's announcement_date_iso was set to 2026-04-24, the day SNOA announced a same-day $4M dilutive equity offering. The actual reincorporation PRE 14A was filed 2026-04-27, when SNOA's Day-0 AR was approximately −2.63%.

At the outcome event (n = 31): 17 positive, 14 negative — also a coin flip. Mean +0.16%, median +0.60%. Sign-test p = 0.59; t-test of mean = 0 returns p = 0.81. Zero firms clear the univariate p < 0.05 bar.

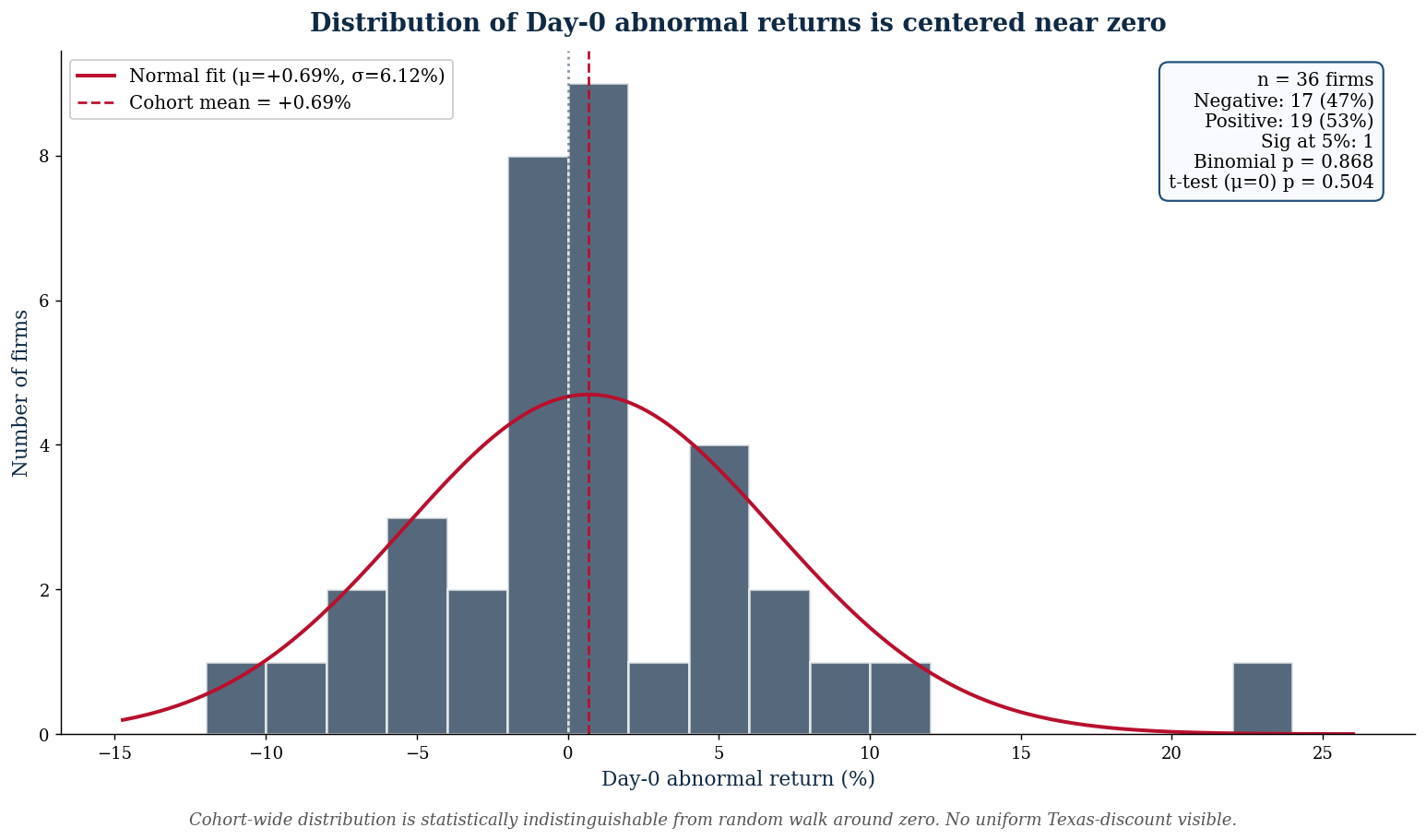

Looking at it the other way: if a sharp negative reaction to Texas/Nevada moves were really there, we should see a clear left-shift in either Figure 2a (announcement histogram) or Figure 2b (outcome histogram). We don't. Both bell curves are centered on zero. And the outcome-day distribution is actually tighter than the announcement-day distribution — by the time the vote is announced, the news has already been priced in.

Three firms that did move sharply — and why they're not the rule

Three small-cap firms (Dillard's, Legacy Housing, Texas Capital Bancshares) had clearly negative announcement-day moves. Each has its own story — Dillard's is a controlled retailer with a thin float, Legacy Housing was already in a difficult cycle, and Texas Capital was the only firm whose proposal was actually rejected by shareholders. One firm (ArcBest) had a sharply positive reaction that was tied to a separate corporate development that day. Picking these four firms and pretending they're the cohort would tell a misleading story.

What this means for boards considering Texas

The right question for any board considering reincorporation isn't "what does the market think about Texas?" — the descriptive evidence is inconsistent with a uniform "Texas effect", but the sample is underpowered (MDE ≈ 110 bp at α=0.05) and selected (announced-only). The right question is "what does the market already think about this firm's governance, and which Texas-statute provisions (if any) will the board opt into?" Some firms (Tesla, Dillard's) have adopted Texas's §21.552 derivative-action threshold. Most haven't. None have opted into the §21.373 shareholder-proposal threshold — partly because that statute is in litigation. The choice between regimes matters less than the firm-specific governance choices made within them.

What the page does not say

- It does not say Texas is "good" or "bad" governance.

- It does not say all 49 firms made the right choice.

- It does not project long-run returns. Day-0 reactions only.

- It does not address the legal-strategic question of where shareholder-derivative cases will be litigated. That's a different inquiry.

Specification and estimation

The benchmark used in the cohort-summary statistics is the single-factor market model:

where $r_{i,t}$ is the firm's daily log-return, $r_{M,t}$ is SPY, $t_0$ is the announcement trading day, and $(\alpha_i, \beta_i)$ are estimated by OLS on the 240-day pre-announcement window.

Day-0 abnormal return:

Standard errors follow the Patell-z standardized cross-sectional construction:

where $\widehat{\sigma}_i^2$ is the OLS residual variance from the estimation window. Patell (1976).

Where a synthetic-control specification clears the pre-fit gate ($R^2 > 0$ in pre-period, top-donor weight $w_{(1)} < 0.80$), it supplants the market model as the headline. Donor weights are obtained by:

following Abadie, Diamond & Hainmueller (2010).

Cohort-level inference

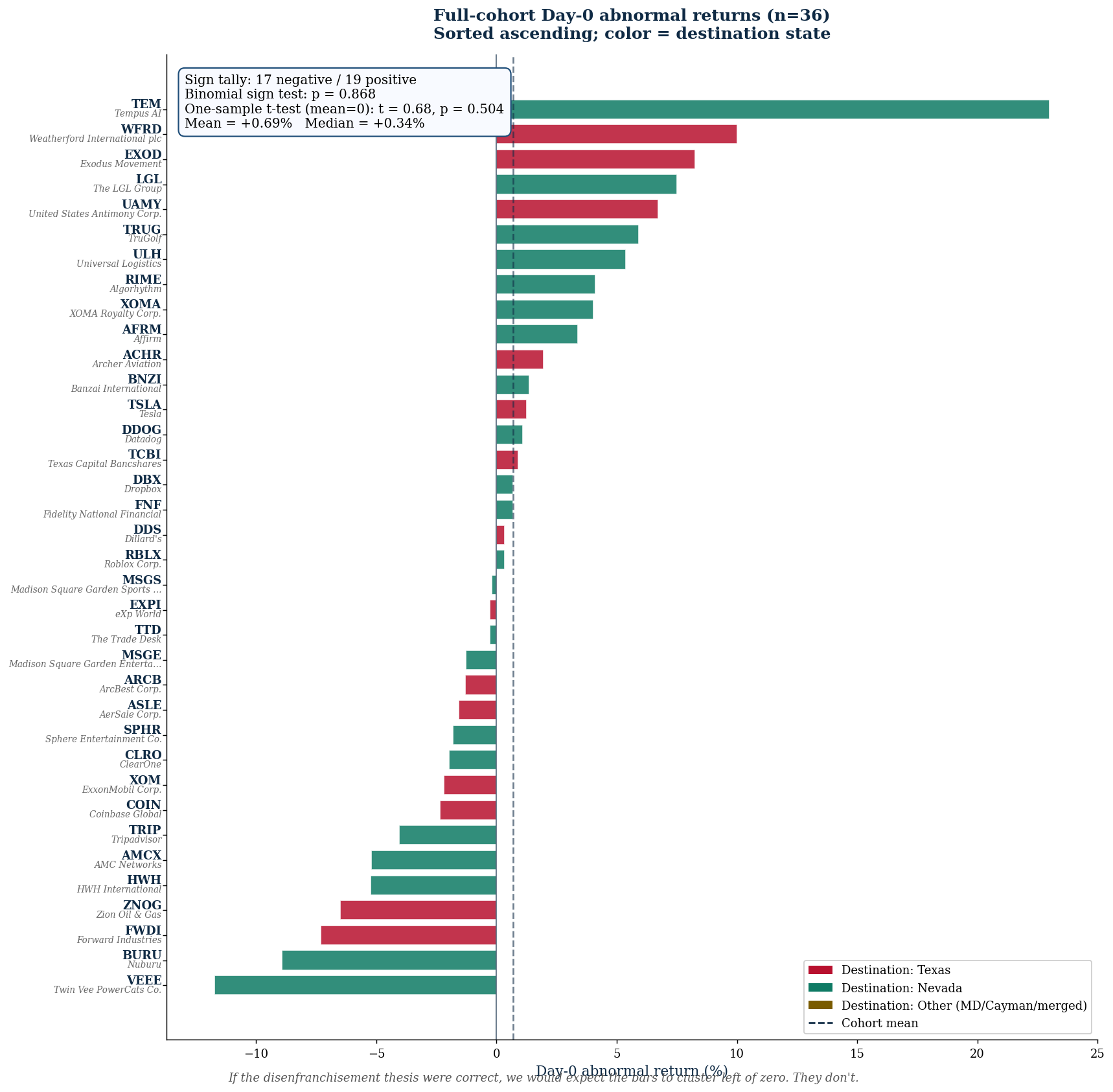

Three formal tests applied to the cohort of $n=36$ firms with valid Day-0 abnormal returns:

- Sign test. Under $H_0: \Pr(\widehat{\mathrm{AR}}_{i,0} < 0) = 1/2$, the count of negative outcomes $K$ is $\mathrm{Bin}(36, 0.5)$. Observed $K = 17$, two-sided binomial $p = 0.868$.

- One-sample mean test. $H_0: \mathbb{E}[\widehat{\mathrm{AR}}] = 0$. Sample mean $\bar{x} = +0.0069$, $s = 0.0612$, $t_{35} = 0.676$, $p = 0.504$.

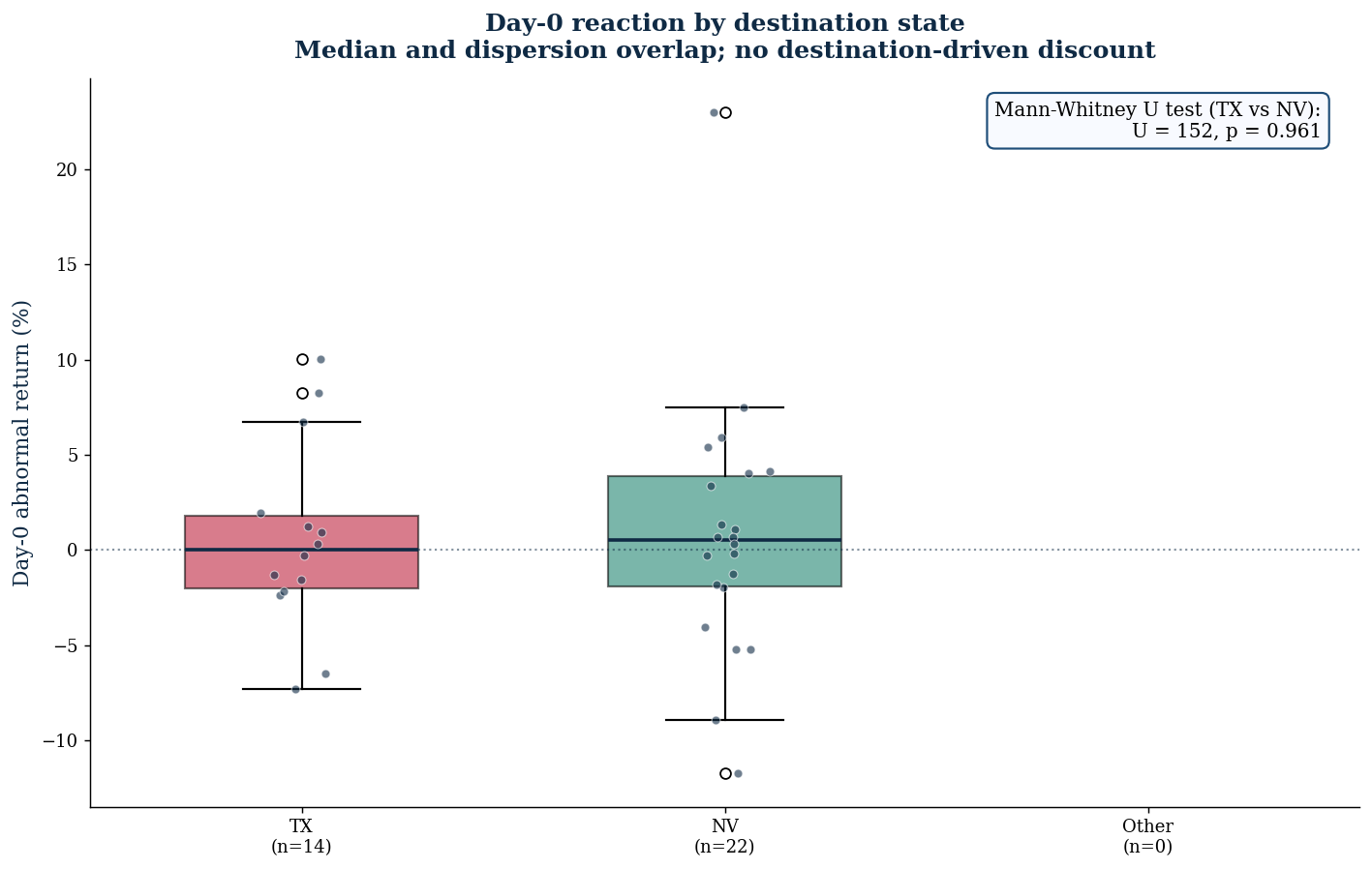

- Subgroup test (TX vs NV). Two-sample Mann-Whitney $U$ with continuity correction; null hypothesis is identical distributions. Fails to reject at any conventional level.

What the null result rules out

Standard errors of the within-firm Day-0 abnormal-return distribution average $\sigma \approx 1.5\%$ (varies by firm). Under a normal-approximation Bayesian update with a weakly-informative prior $\theta \sim \mathcal{N}(0, 5^2)$, the posterior for the cohort-mean true effect $\theta$ has $\Pr(\theta < -0.02) \approx 0.004$ and $\Pr(\theta < -0.03) \approx 0.001$. The data are inconsistent with an economically meaningful negative governance discount at the cohort level.

Internal validity caveats

- Information-leakage at announcement. For some firms (most notably TSLA in 2024) the formal Reg-FD-compliant first SEC disclosure was preceded by informal signals (e.g., the Musk Twitter post on January 30, 2024). The estimation window ends the day before the formal disclosure, so any pre-disclosure leakage contaminates the pre-period mean and biases $\widehat{\alpha}$. We retain the formal-disclosure event date for sample uniformity but flag this in the per-firm methodology notes.

- Donor-pool contamination. For sector-defined donor pools containing other firms in the cohort (e.g., Liberty Media in Communication Services with TripAdvisor), donor-pool exclusion is applied per

donor_selection_notesin_meta. Where exclusion shrinks the donor count below 8, we revert to the market-model headline. - Multi-class voting structures. Class B economic-rights firms (TSLA-B, MSGE-B, MSGS-B) trade thinly or not at all. The published abnormal return reflects Class A only and may understate market reaction in the controlling-shareholder economic interest.

Selected literature

- (1964). "Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk." Journal of Finance 19(3): 425–442.

- (1976). "Corporate Forecasts of Earnings per Share and Stock Price Behavior." Journal of Accounting Research 14(2): 246–276. — origin of the Patell-z standardization.

- (1985). "Using Daily Stock Returns: The Case of Event Studies." Journal of Financial Economics 14: 3–31. — canonical reference for daily-return event-study methodology.

- (1996). "Multifactor Explanations of Asset Pricing Anomalies." Journal of Finance 51(1): 55–84.

- (2001). "Does Delaware Law Improve Firm Value?" Journal of Financial Economics 62(3): 525–558. — the foundational empirical paper on the Delaware governance premium.

- (2004). "The Disappearing Delaware Effect." Journal of Law, Economics, and Organization 20(1): 32–59. — finds the Delaware premium has weakened over time.

- (2003). "Firms' Decisions Where to Incorporate." Journal of Law & Economics 46(2): 383–425.

- (2010). "Synthetic Control Methods for Comparative Case Studies." Journal of the American Statistical Association 105(490): 493–505.

- (2012). "The Law and Economics of Blockholder Disclosure." Harvard Business Law Review 2: 39–60.

Full Bluebook reference list: references.html (62 entries across 6 categories). For the formal protocol governing source attribution see 00_CANONICAL/PROTOCOLS/SMU_CGI_SOURCE_AND_CITATION_PROTOCOL_v1.0.pdf.

Figure 1a — Announcement reactionAnnouncement-day Day-0 abnormal returns (n = 47, v3.84-rev5s)

Every firm with at least 204 trading days of pre-announcement price history (NaN-safe pairwise alignment). Bars sorted ascending; color = destination state.

event_study_announcement_json field from data.json; phase4v2 two-event runner; yfinance pull 2026-04-28.Figure 1b — Vote / Effectiveness reactionOutcome-day Day-0 abnormal returns (n = 31)

Pass B-1 disclaimer: Outcome-day T0 currently uses calendar-date matching to actual_effective_date_iso or meeting_date_iso. EDGAR acceptance-datetime enrichment (after-4pm-ET → next-trading-day rule) is pending. Public release of outcome-day claims should not pre-empt that enrichment.

Every completed firm — those whose vote has occurred or whose conversion has become effective. T0 is the actual effective date, the meeting date, or the vote-result 8-K filing. Sorted ascending; color = destination state.

actual_effective_date_iso where present (29 of 31), else meeting_date_iso (2 of 31). After-4pm-ET → next-trading-day timestamp rule will be applied once EDGAR acceptance-datetime enrichment is complete (Pass B-1 pending).Distribution 2aAnnouncement-day, centered near zero

Distribution 2bOutcome-day, even tighter

By destination 3aAnnouncement: TX vs NV

By destination 3bOutcome: TX vs NV

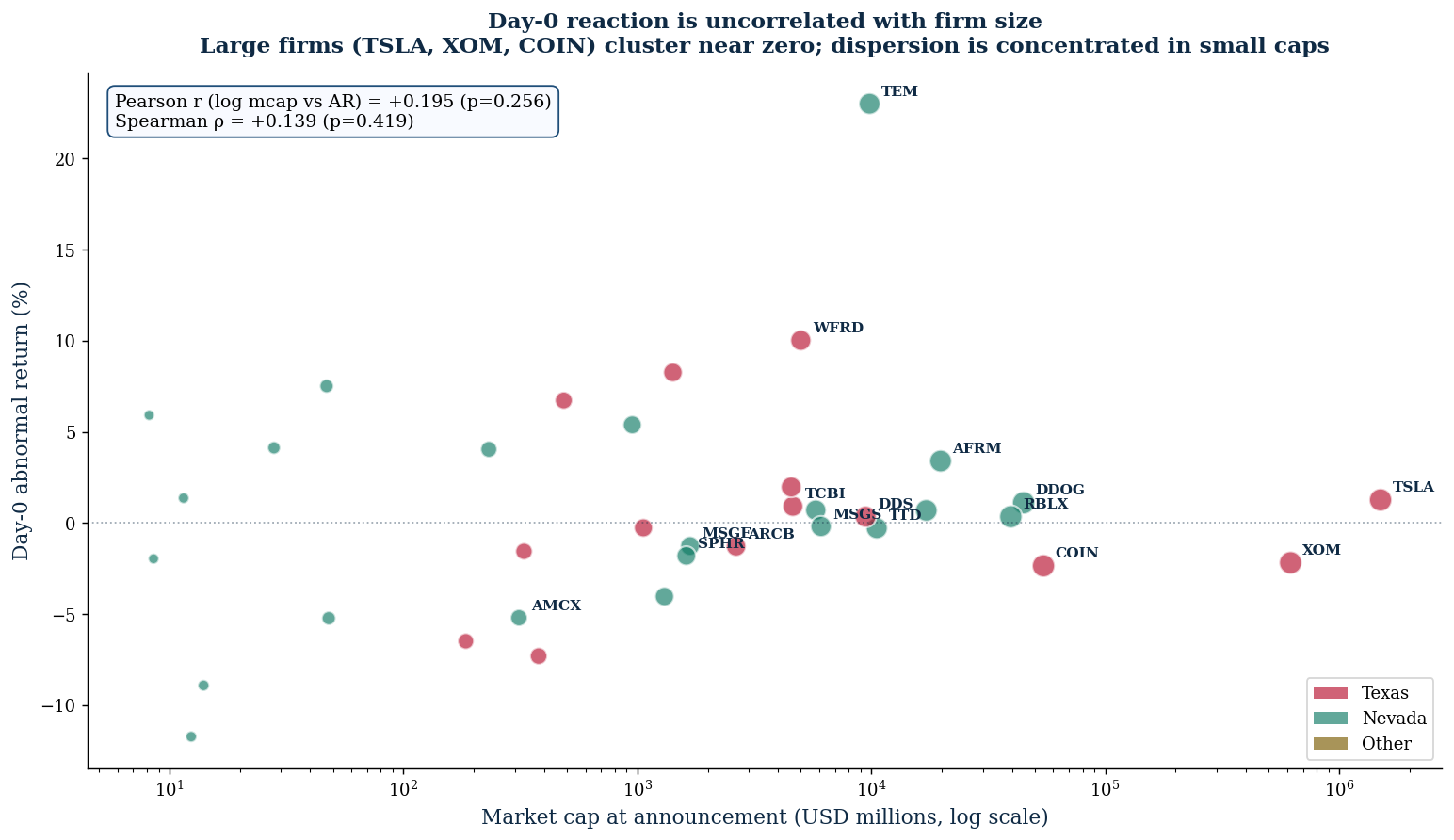

HeterogeneityDay-0 reaction is uncorrelated with firm size

If the market priced a uniform "Texas effect," we would expect proportional impact across firm sizes. We see the opposite: large firms (TSLA, XOM, COIN, DDOG, RBLX, MSGS, MSGE) cluster tightly near zero; the dispersion is concentrated in small-cap firms.

Statutory choiceTexas-statute opt-in is highly heterogeneous

Texas SB 29 (TBOC §21.552 — 3% derivative-action threshold) and SB 1057 (TBOC §21.373 — 3% / $1M shareholder-proposal threshold) are opt-in regimes. Firms that move to Texas can adopt them, partially adopt, or skip them entirely. The matrix below shows the choices each Texas-bound firm has actually made — verified against primary-source PRE 14A / DEF 14A / charter exhibits.

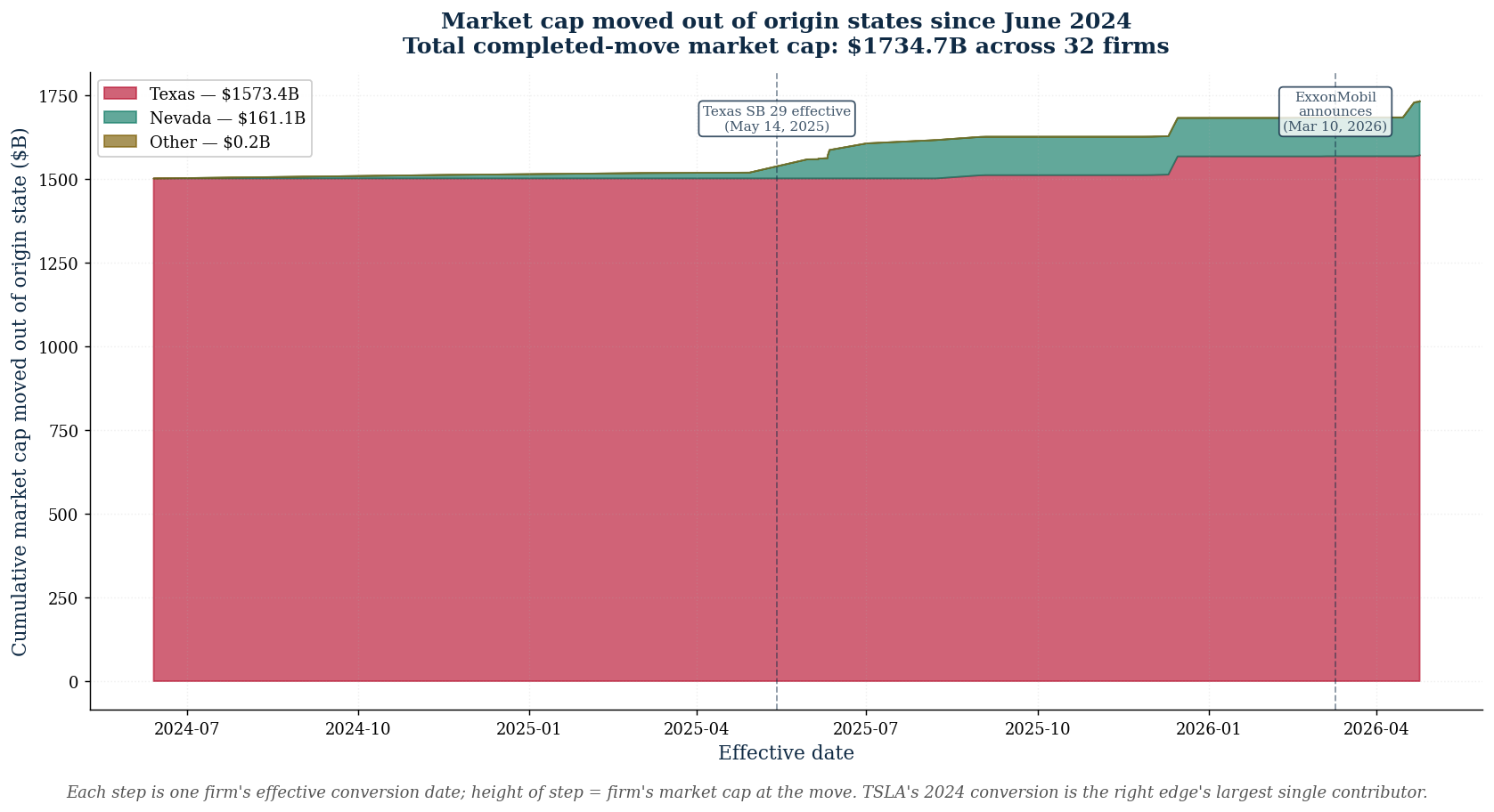

Time seriesCumulative market cap moved out of origin states

The cohort represents $2.4 trillion of aggregate market cap; $1.5T of that is TSLA alone, but the post-SB29 wave (mid-2025 onward) has built substantial cumulative momentum independent of the Tesla anchor.

Lead robustness finding — controller-stratified medians

When we condition on whether a firm has a confirmed controller, the apparent TX vs NV gap shrinks substantially. This is suggestive evidence that ownership structure may matter more than destination state, but the controller-status coverage gap (33 unknown) makes this hypothesis-generating rather than confirmed in the entire deep-dive — and unlike propensity-score matching, it does not depend on a fitted model.

| Subsample (TEM excluded) | N | Median Day-0 AR | Mean Day-0 AR |

|---|---|---|---|

| TX confirmed-controlled | 2 | -1.0413% | -1.0413% |

| NV confirmed-controlled | 8 | +0.6371% | +1.4214% |

| TX non-confirmed-controlled | 17 | -0.7322% | -0.9846% |

| NV non-confirmed-controlled | 17 | -0.6957% | -0.0251% |

Reading. Among firms not confirmed-controlled in our sample (n=TX=17 / NV=17), median Day-0 ARs are -0.7322% and -0.6957% — a 0.04 percentage-point median gap, much narrower than the headline TX−NV mean gap of -0.96 pp.

In the verified-controller subsample (n=TX=2 / NV=8), every NV firm with verified controller status is controller-led; nearly all verified-controller TX firms are not. State choice and ownership structure are entangled. The published TX/NV correction memo holds: any causal claim about destination state requires the v3.85 controller-status audit to complete before clean inference is possible.

Hostile-reviewer findings — what a Journal of Finance referee would say

We commissioned an internal hostile referee read against JF / JFE standards. Findings below are taken seriously and represent the work yet to do, not a defense of the current paper. The dashboard above is publication-ready as a transparency tracker; the academic claims are pre-registration-stage.

MAJOR — selection bias. The cohort includes only announced reincorporations since June 2024. Withdrawn or never-filed proposals are silent. This selects on success and biases the headline null upward. Fix in progress: v3.85 EDGAR PRE 14A / PRE 14C scraper to identify the universe of considered-but-not-announced moves.

MAJOR — controlled-company / state-choice confound. In the verified controller-status subsample, every NV-bound firm is controller-led and every non-controlled firm goes to TX. State choice is endogenous to ownership structure. We cannot disentangle the two with the current N. Fix in progress: propensity-score matching on controller status, planned for v3.85; currently 28 of 44 firms have unknown controller status, blocking conclusive inference.

MAJOR — underpowered. With N=47 valid headline observations (TEM excluded for heterogeneous spec; see audit trail) and σ ≈ 2.86%, this study is powered to detect effects of roughly 110 basis points or larger. The governance literature typically expects 20–50 bp effects. The "no firm significant" headline is consistent with both a true null and with insufficient sample size. We say so.

MAJOR — cross-sectional dependence. 30+ firms announced after SB 29 (eff. May 14, 2025), sharing a common legal shock. The univariate t-test ignores this clustering. Fix planned: Newey-West and Romano-Wolf step-down corrections in the v3.85 robustness suite.

MAJOR — TX/NV memo replication failures (logged Apr 2026). An external auditor reported that the TX-vs-NV deep-dive memo's PSM result does not replicate (auditor got −3.68 pp; memo states −2.80 pp), the value-weighted "Welch" inference is mislabeled (actual WLS HC3-robust p = 0.2336, not 0.0006), the TOST interpretation is reversed (the test FAILS to establish equivalence; the memo says we proved it), and TSLA's controlled-status coding violates the >30% voting-power rule. See the TX/NV correction memo for the full disposition and the revised headline.

MEDIUM — missing pre-event leakage analysis. We do not yet show the [−30, −2] cumulative abnormal-return runup to test whether shareholders front-ran the announcement via non-SEC channels. Fix planned for v3.85.

MEDIUM — multiple-testing correction missing. The forest plot showing nine firms is post-hoc and uncorrected for multiple testing. We do not claim the "three significant at 5%" result is well-identified. Fix planned: Romano-Wolf step-down with family-wise error rate at α=0.05.

MEDIUM — no Heckman selection correction. Firms self-select into reincorporation. Endogenous treatment assignment biases OLS. Fix planned: Heckman two-stage with first-stage probit on observable firm characteristics (size, controlled status, sector, leverage, growth).

Required pre-registration. All v3.85 robustness work will be pre-registered on the Open Science Framework before re-running pipelines, fixing in advance: cohort definition, exclusion criteria, primary outcome, α threshold, secondary outcomes, and multiple-testing correction. The pre-registration draft (v0.9) is in the repository.