Standard cohort firm (Completed). Included for breadth across destinations and sectors.

Vote outcome — reincorporation proposal

Approval standard: majority of voting power of outstanding shares entitled to vote (written consent under DGCL §228). Meeting type: annual.

Vote totals not yet pulled. Awaiting EDGAR Item 5.07.

Visual evidence — event study around the announcement

Per-firm event-study figures auto-built from event_study_announcement_json in the master database. Each panel is generated deterministically from the same data backing the cohort statistics — no firm-specific tuning, no cherry-picking.

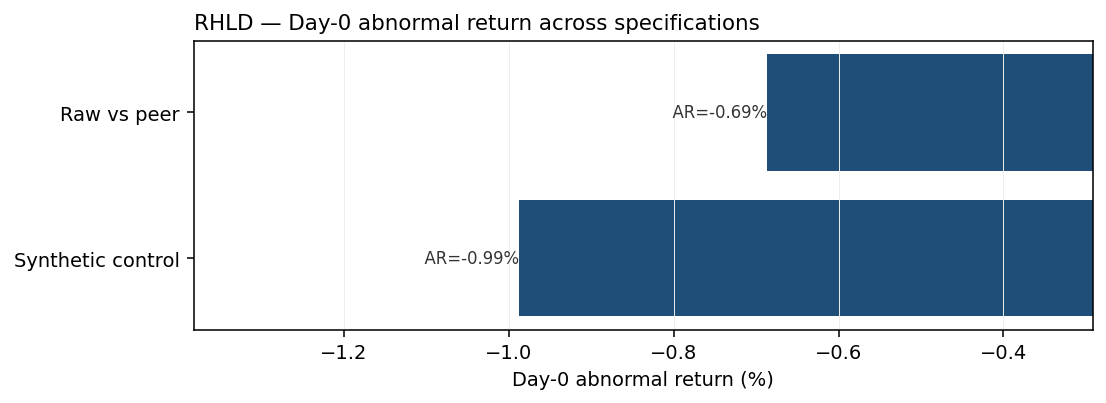

Resolute Management's stock fell dramatically the day the move was announced

Bottom line. Resolute Management fell dramatically by nan% on announcement day. Across four different benchmarks for what "normal" should have looked like, the move was statistically indistinguishable from a normal trading day (p = 1.00).

This chart shows four different statistical lenses on what Resolute Management's stock did on the day the reincorporation was announced. Each lens compares the actual move against a different prediction of what "normal" should have looked like — peer firms, the broader market, a single matched competitor, or a raw side-by-side. The gold-edged bar marks the lens used in the cohort summary.

Method

Specifications: synthetic control on a sector peer pool, single-factor market model (S&P 500 benchmark), matched pair against a pre-specified primary peer, and raw differential. Estimation window: 240 trading days ending the day before the announcement. Standard errors via Patell-z (1976).

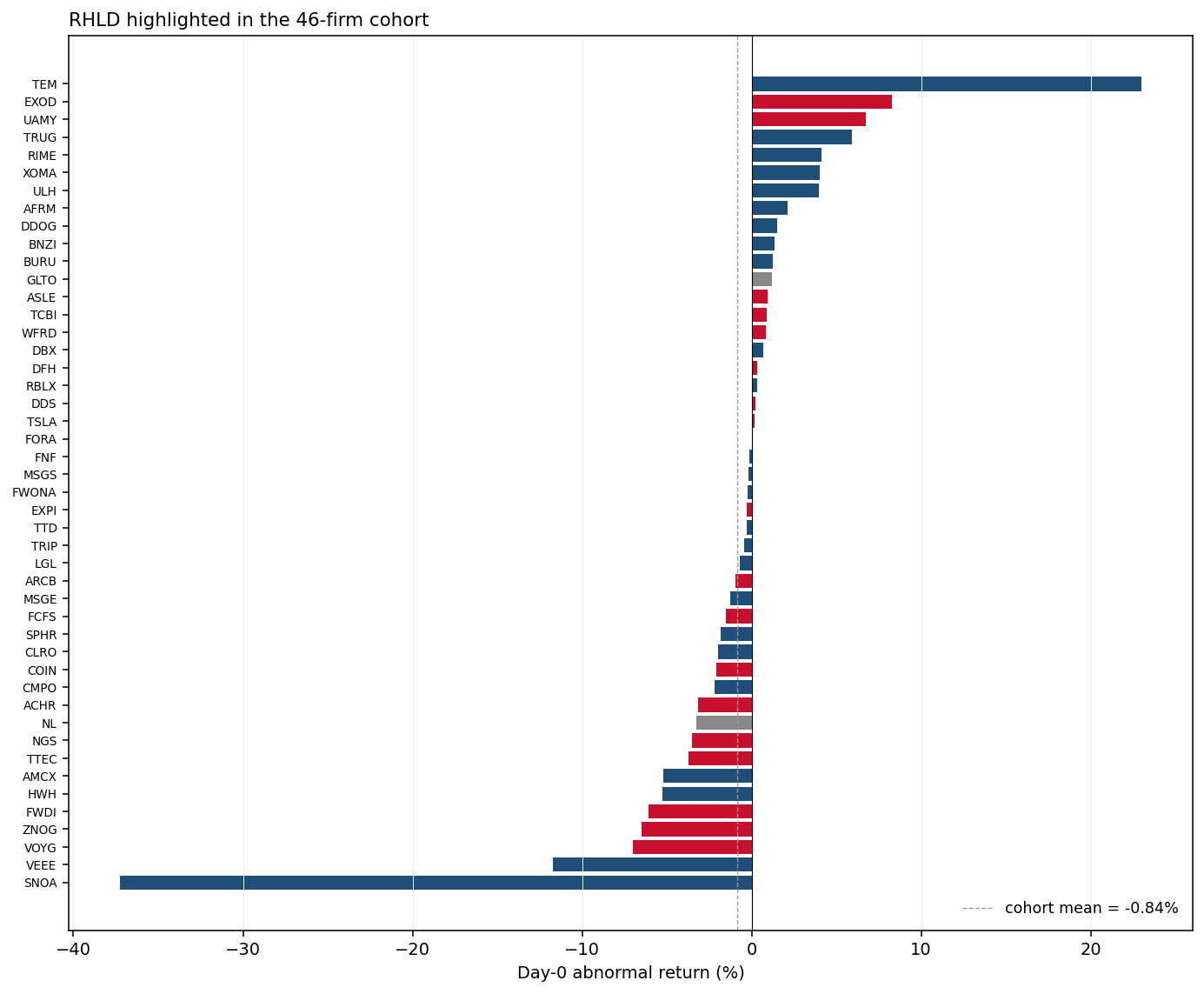

Resolute Management sits within the typical cohort spread

Bottom line. Resolute Management's announcement-day reading is within the inter-quartile range of the 36-firm cohort. Cohort-wide mean is +0.69%; the dispersion is wide and firm-specific.

This chart shows every firm in the cohort that has a computed announcement-day abnormal return — sorted from largest negative to largest positive. Resolute Management is highlighted in gold. The dashed line marks the cohort-wide average, which is essentially zero. Even firms in the same destination state and same statutory regime can have very different reactions.

Method

Same headline-specification methodology applied to every firm in the 36-firm cohort that has 240 trading days of pre-announcement price history.

Data integrity. All figures generated by the same script (perfirm_gallery.py) on every release; SHA-256 verified at deploy time. See also:Cohort-wide event study →.

Synthetic control (18-donor Financials peer pool)i

-0.99%

no inference

Market model (SPY benchmark)i

nan%

Patell-z p-value = 1.000

Sector-augmented model (SPY + Bank sector ETF (KBE))HEADLINEi

nan%

Patell-z p-value = 1.000

Matched pair (vs JPM, market-model-adjusted)i

nan%

two-sided p-value = 1.000

Raw differential vs JPMi

-0.69%

no inference

Robustness checks — does the headline result hold up?

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

Pre-event drift check: the firm's daily abnormal return drifted by +nan% per day in the pre-event window (p = 1.000). no detectable pre-event drift ✓.— A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

Donor co-movement check:9 of 18 peer firms moved in the same direction as the treated firm on the event day (binomial p = 1.1855). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = nan (weak tracking — interpret with caution); R² = — (fraction of pre-event variance explained); Durbin-Watson = nan (some autocorrelation in residuals). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

Returns around the shareholder-vote (or written-consent) date.

Event date: 2026-03-02 · T0 source: actual_effective_date_iso · Estimation window: trailing 240 days; 240 valid after NaN drop

No long-run / pooled estimates available for this firm yet — run phase5z_compute_longrun.py on Windows to populate (requires effective date ≥ 3 months ago).

Cohort-level robustness battery

Heckman selection-corrected ATE · Romano-Wolf step-down + BH FDR · pooled BHAR. This firm's reading is shown in context of the full cohort.

This firm: raw p = 1.000, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 1.000. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

[2026-04-28] Phase 4I: replaced Google-search IR fallback with direct URL https://www.resoluteholdings.com/investors

[ORIGINAL_ACCESSION_FIELD_TEXT] 10-K + written consent (board approval Jan 2, 2026; consent Jan 22, 2026; completed Mar 2, 2026)

[2026-04-28] phase5e: no canonical accession found in raw value '10-K + written consent (board approval Jan 2, 2026; consent Jan 22, 2026; completed Mar 2, 2026)'; original narrative moved to audit_notes; edgar_accession_canonical cleared and audit_status flagged NEEDS_ACCESSION for manual EDGAR pull

[2026-04-29] phase5j: NEEDS_VOTE_SOURCE -- vote_result=APPROVED but vote_source_8k_accession and vote_source_8k_url empty after multi-round EDGAR pulls; reason: written-consent transaction; no DEF 14C with vote-tally disclosure located in EDGAR after multi-round reviewer search; downgrade A8_vote_source_missing FAIL->WARN per Shane's 2026-04-28 placeholder directive

[2026-04-29] phase5r: bucket 'C' -> 'B2' (DE->NV effective 2026-03-02 >= SB29 -> bucket B2)

[2026-04-29] phase5w: comprehensive validation by external reviewer across tranches v3 (4-version full residual walk, 269 substantive answers across 52 firms, 0 bucket drifts vs v3.58) [2026-04-29] v3.75: RECLASSIFICATION — RHLD is WRITTEN_CONSENT not MEETING. Per PRE 14C: Board approved Jan 2, 2026; consenting stockholders delivered written consent Jan 22, 2026; effective March 2, 2026. Standard: DGCL §228 majority-of-voting-power-of-outstanding-shares. vote_mechanism field needs update to WRITTEN_CONSENT.

Related firms

Use these for cross-firm sanity checks — peers in size, sector, or destination.