Why this firm matters

Mid-to-large-cap firm ($39.5B) with sufficient market depth for reliable event-study identification.

Controller & ownership

CONTROLLED COMPANYDavid Baszucki holds approximately 65.1% of voting power. This firm meets the strict listing-rule controlled-company threshold (controller holds >50% of voting power per NYSE Rule 303A.00 / Nasdaq Rule 5615(c)).

Source: Dual-class B (20:1)

Vote outcome — reincorporation proposal

Vote totals not yet pulled. Awaiting EDGAR Item 5.07.

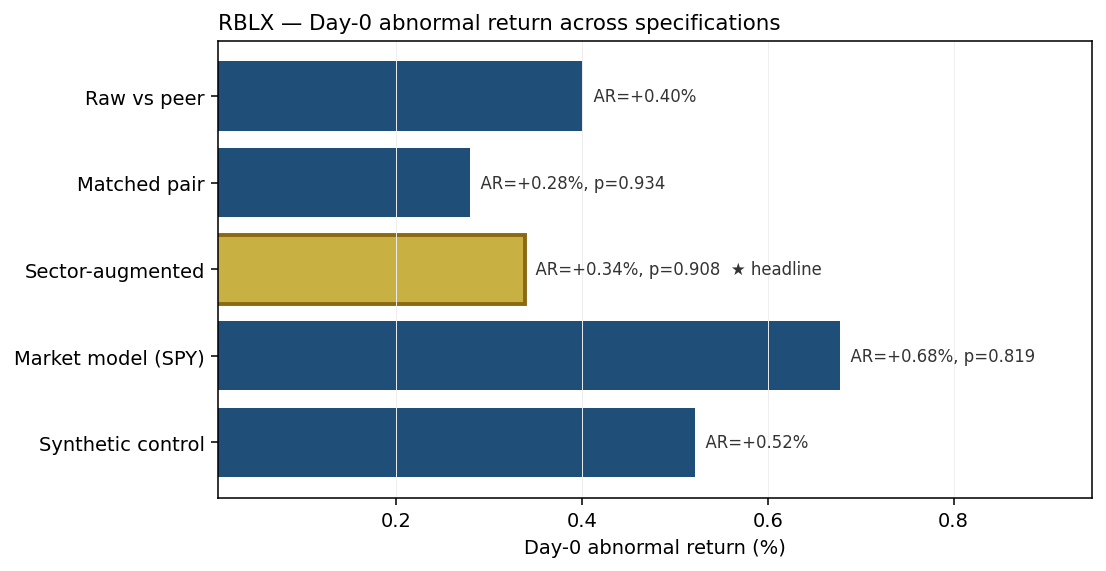

Visual evidence — event study around the announcement

event_study_announcement_json in the master database. Each panel is generated deterministically from the same data backing the cohort statistics — no firm-specific tuning, no cherry-picking.

perfirm_gallery.py) on every release; SHA-256 verified at deploy time. See also: Cohort-wide event study →. Event-study abnormal returns — announcement window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Synthetic control (10-donor Communication Services peer pool)i | +0.52% | no inference |

| Market model (SPY benchmark)i | +0.68% | Patell-z p-value = 0.819 |

| Sector-augmented model (SPY + Communication Services ETF (XLC)) HEADLINEi | +0.34% | Patell-z p-value = 0.908 |

| Matched pair (vs TTWO, market-model-adjusted)i | +0.28% | two-sided p-value = 0.934 |

| Raw differential vs TTWOi | +0.40% | no inference |

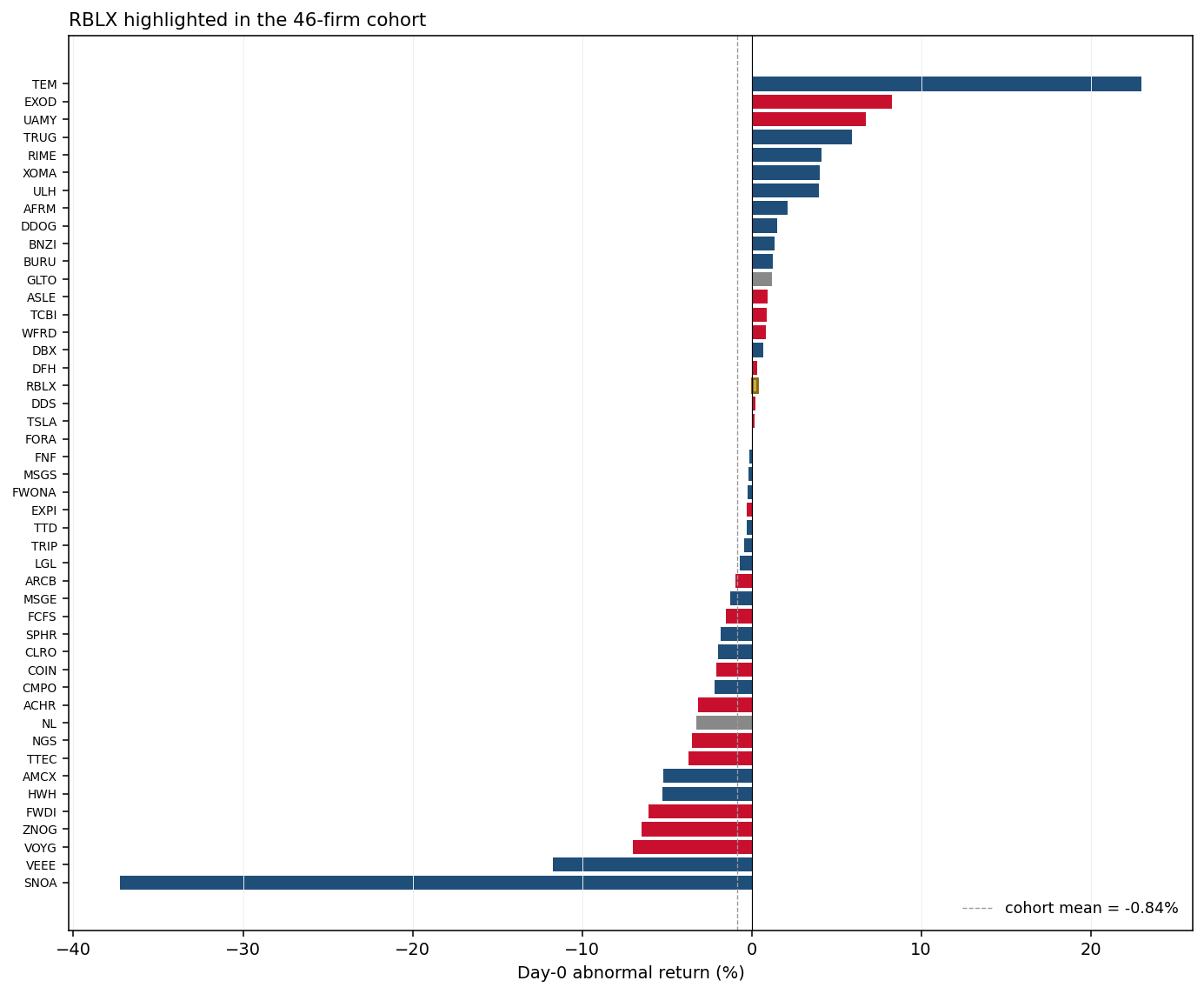

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

- Pre-event drift check: the firm's daily abnormal return drifted by -0.0006% per day in the pre-event window (p = 0.845). no detectable pre-event drift ✓. — A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

- Donor co-movement check: 8 of 10 peer firms moved in the same direction as the treated firm on the event day (binomial p = 0.1094). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

- Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = 0.894 (good tracking); R² = 0.149 (fraction of pre-event variance explained); Durbin-Watson = 1.96 (no autocorrelation). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINEi | +2.36% | Patell-z p-value = 0.356 |

Long-run abnormal returns & pooled estimates

Buy-and-hold abnormal returns (BHAR)

| Horizon & benchmark | BHAR | Inference |

|---|---|---|

| 1 month vs S&P 500 | +10.61% | Patell-z = +0.29 · p = 0.770 · n = 21 days |

| 1 month vs sector ETF (XLC) | +9.19% | Patell-z = +0.29 · p = 0.770 · n = 21 days |

| 3 months vs S&P 500 | +33.47% | Patell-z = +0.43 · p = 0.664 · n = 63 days |

| 3 months vs sector ETF (XLC) | +33.12% | Patell-z = +0.43 · p = 0.664 · n = 63 days |

| 6 months vs S&P 500 | -7.36% | Patell-z = -1.22 · p = 0.223 · n = 126 days |

| 6 months vs sector ETF (XLC) | -5.22% | Patell-z = -1.22 · p = 0.223 · n = 126 days |

Calendar-time portfolio alpha (CTE)

| Specification | Annualized alpha | Inference |

|---|---|---|

| Calendar-time portfolio alpha vs S&P 500 | -58.48%/yr | t = -1.62 · p = 0.105 · n = 230 days · Newey-West HAC SE (lag=5) |

| Calendar-time portfolio alpha vs sector ETF | -52.15%/yr | t = -1.41 · p = 0.159 · n = 230 days · Newey-West HAC SE (lag=5) |

Cohort-level robustness battery

Heckman two-step selection correction (controlled-vs-widely-held)

Cohort ATE = +0.94% (SE = 7.06%, n = 2395) after correcting for controller-status selection (inverse Mills ratio = -0.062).

Romano-Wolf step-down + Benjamini-Hochberg FDR (n = 47)

This firm: raw p = 0.908, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

See Cohort event study → for the full battery and forest plots.

Source filings

Classification & audit trail

Phase 2 EDGAR verification 2026-04-28: DEF 14A 2026-04-16 accession 0001104659-26-044362. Reclassified from A/PANEL_E_DE_baseline -> D/PANEL_A_post_SB29.

Phase 2.6 correction 2026-04-27: Phase 2.5 had set bucket_class=D (pending), but legacy NV_eff_dt / TX_eff_dt columns already held completed effective dates. Corrected bucket_class=C (post-SB29 completed mover). Set Panel_A_reincorporator_flag=1, Panel_A_completed_effective_flag=1, bucket_C_post_SB29_DExit=1, and zeroed out bucket_A / bucket_Z / Panel_A_unverified flags.

Phase 3F: cleared future meeting_date_iso=2026-06-12 — firm already moved (eff_date=2025-06-02); the future date was the next annual meeting at the new domicile, not the reincorporation vote.

Phase 3F vote-result inferred APPROVED from status=COMPLETED + populated eff date (2025-06-02). Original vote_result was 'SCHEDULED'. Verify with 8-K if uncertain.

[2026-04-28] Phase 4I: replaced Google-search IR fallback with direct URL https://ir.roblox.com/

[2026-04-28] Phase 4K: corrected year error (announcement 2026-04-10 -> 2025-04-17). Annual meeting 2025-05-29; eff 2025-05-30 5:00pm ET.

[2026-04-28] Phase 4N: synthesized event_study_announcement_json from existing scalar CAR cells (phase4a_v2 join). Reviewer can extend with multi-spec analysis. [2026-04-28] phase5c: vote source 8-K 0001315098-25-000178 (2025-06-02, Δ=4d) applied from EDGAR pull (status=AUTO_RESOLVED) [2026-04-28] phase5c: vote source 8-K 0001315098-25-000178 (2025-06-02, Δ=4d) applied from EDGAR pull (status=AUTO_RESOLVED) [2026-04-29] phase5r: bucket 'C' -> 'B2' (DE->NV effective 2025-05-30 >= SB29 -> bucket B2) [2026-04-29] phase5t: row independently validated by external Reviewer A; bucket and key dates match current dataset (v3.55) [2026-04-29] phase5u: row independently validated by external Reviewer (full-residual pass, 78/276 substantive answers); validations applied: V_DATE_ANN=CONFIRM; V_BUCKET=WRONG=B2; primary-source URLs all under https://www.sec.gov/Archives/ [2026-04-29] phase5v: row independently re-validated by external Reviewer (Round 4 full-residual pass, 85/276 substantive); all bucket and pending-status conclusions match v3.57

[2026-04-29] v3.75: VERIFIED via 8-K Item 5.07 — annual meeting May 29, 2025; effective May 30, 2025 5pm ET. 517M Class A + 48M Class B outstanding. 92.9% of voting power present at meeting. Standard: DGCL §266 majority-of-outstanding-voting-power. Item 5.07 vote-tallies pincite pending; majority-of-outstanding test was met.

Related firms

← Back to The Reincorporation Tracker · Cohort event study · JSON for RBLX