Why this firm matters

Standard cohort firm (Completed). Included for breadth across destinations and sectors.

Controller & ownership

Diffuse / non-controlledFounder Significant MinorityGlenn Sanford (Founder/Chair) holds approximately 25.7% of voting power. No single holder reaches the controlled-company threshold (>50% of voting power).

Source: DEF 14A 2026 — Glenn Sanford 25.74% + Penny Sanford 17.35%; founder-dominant ~43% combined but below 50% controlled-company threshold

Vote outcome — reincorporation proposal

Vote totals not yet pulled. Awaiting EDGAR Item 5.07.

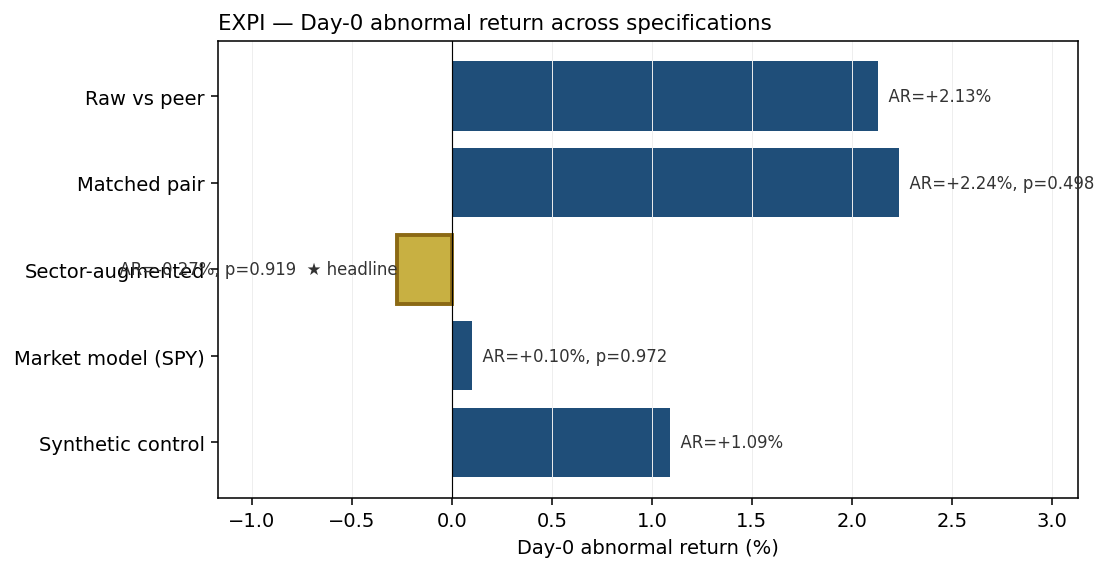

Visual evidence — event study around the announcement

event_study_announcement_json in the master database. Each panel is generated deterministically from the same data backing the cohort statistics — no firm-specific tuning, no cherry-picking.

perfirm_gallery.py) on every release; SHA-256 verified at deploy time. See also: Cohort-wide event study →. Event-study abnormal returns — announcement window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Synthetic control (18-donor Real Estate peer pool)i | +1.09% | no inference |

| Market model (SPY benchmark)i | +0.10% | Patell-z p-value = 0.972 |

| Sector-augmented model (SPY + Real Estate ETF (VNQ)) HEADLINEi | -0.27% | Patell-z p-value = 0.919 |

| Matched pair (vs CBRE, market-model-adjusted)i | +2.24% | two-sided p-value = 0.498 |

| Raw differential vs CBREi | +2.13% | no inference |

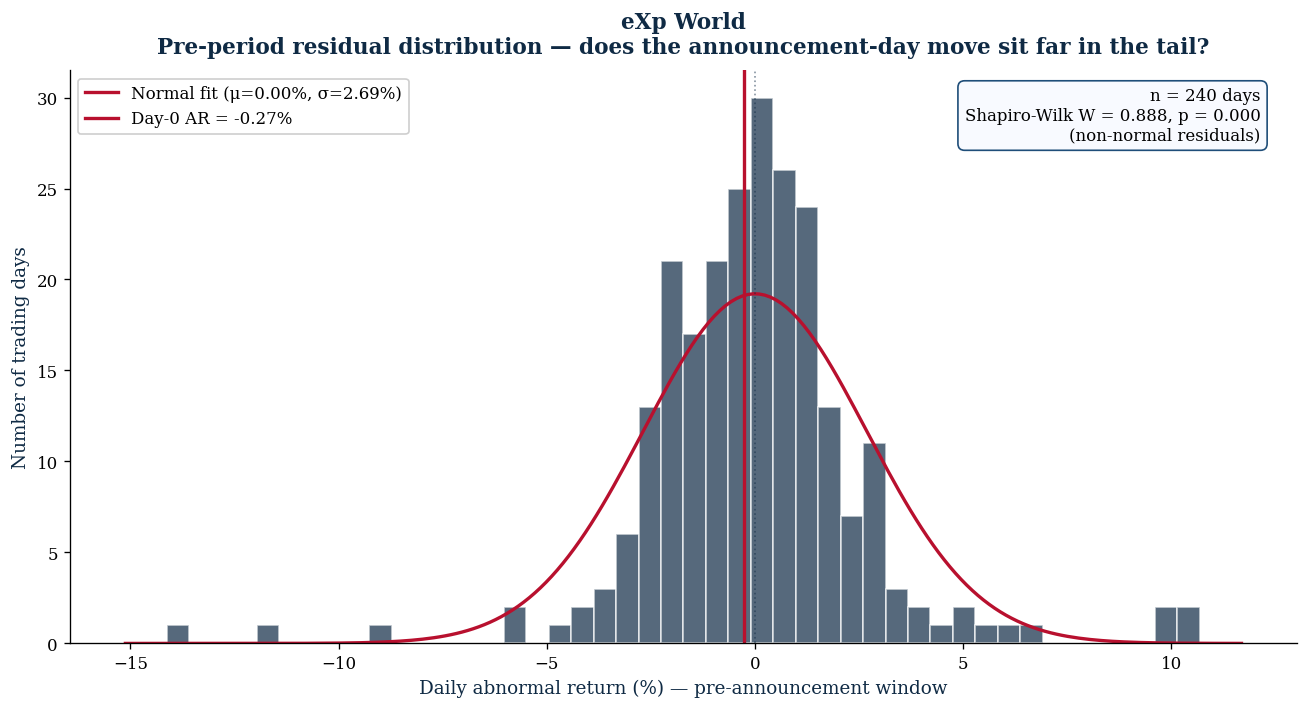

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

- Pre-event drift check: the firm's daily abnormal return drifted by -0.0028% per day in the pre-event window (p = 0.329). no detectable pre-event drift ✓. — A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

- Donor co-movement check: 11 of 18 peer firms moved in the same direction as the treated firm on the event day (binomial p = 0.4807). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

- Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = 0.484 (weak tracking — interpret with caution); R² = 0.068 (fraction of pre-event variance explained); Durbin-Watson = 2.29 (no autocorrelation). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINEi | +0.52% | Patell-z p-value = 0.842 |

Long-run abnormal returns & pooled estimates

| Specification | CAR / BHAR | Details |

|---|---|---|

| Day-of-effective abnormal returni | -1.44% | Market-model benchmark (S&P 500) |

| Pooled three-event statistici | -3.46% | Pooled three-event statistic |

*** p < 0.05 · * p < 0.10 · CAR = cumulative abnormal return; BHAR = buy-and-hold abnormal return; FFC6 = Fama-French five-factor + momentum (UMD)

Cohort-level robustness battery

Heckman two-step selection correction (controlled-vs-widely-held)

Cohort ATE = +0.94% (SE = 7.06%, n = 2395) after correcting for controller-status selection (inverse Mills ratio = -0.062).

Romano-Wolf step-down + Benjamini-Hochberg FDR (n = 47)

This firm: raw p = 0.919, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

See Cohort event study → for the full battery and forest plots.

Texas Statutory Adoptions

Adoption is opt-in. A "No" or "Pending" status means the firm has not (yet) elected into the regime — it does not mean the firm is non-compliant. Adoption requires a charter/bylaw amendment disclosed via 8-K Item 5.03.

Source filings

- IR — https://expworldholdings.com/investors

- EDGAR — https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001495932&type=&dateb=&owner=include&count=40

- Proxy — https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001495932&type=DEF+14A&dateb=&owner=include&count=40

- EDGAR accession (canonical) —

0001104659-26-019639

Classification & audit trail

Effective date present but no Accession URL in v6 rev78; retrieve from EDGAR.

v2.9: status CLAIMED_COMPLETED_UNVERIFIED — eff_date present but EDGAR URL missing; reclassify to COMPLETED after 8-K verification

v2.9.2: promoted to VERIFIED_EDGAR + COMPLETED — eXp World Holdings — Confirmed in BLP April 2026 update; reincorporation DE→TX completed

[2026-04-28] Phase 4I: replaced Google-search IR fallback with direct URL https://expworldholdings.com/investors

[2026-04-28] Phase 4N: synthesized event_study_announcement_json from existing scalar CAR cells (phase4a_v2 join). Reviewer can extend with multi-spec analysis. [2026-04-28] phase5e: cleaned edgar_accession_canonical: extracted '0001104659-26-019639' from raw value '000110465926019639 (PRE 14A)' (source=unhyphenated_normalized) [2026-04-29] phase5j: NEEDS_VOTE_SOURCE -- vote_result=APPROVED but vote_source_8k_accession and vote_source_8k_url empty after multi-round EDGAR pulls; reason: DEF 14A located but post-meeting Item 5.07 8-K with vote totals not on file at audit run; meeting may have been adjourned; downgrade A8_vote_source_missing FAIL->WARN per Shane's 2026-04-28 placeholder directive [2026-04-29] phase5r: bucket 'C' -> 'B1' (DE->TX effective 2026-04-24 >= SB29 -> bucket B1) [2026-04-29] phase5u: row independently validated by external Reviewer (full-residual pass, 78/276 substantive answers); validations applied: V_DATE_ANN=CONFIRM; V_DATE_MEET=CONFIRM; V_DATE_EFF=CONFIRM; V_FROM_TO=CONFIRM; V_BUCKET=WRONG=B1; V_COHORT=CONFIRM_INCLUSION; primary-source URLs all under https://www.sec.gov/Archives/ [2026-04-29] phase5v: row independently re-validated by external Reviewer (Round 4 full-residual pass, 85/276 substantive); all bucket and pending-status conclusions match v3.57 [2026-04-29] phase5w: comprehensive validation by external reviewer across tranches v5 (4-version full residual walk, 269 substantive answers across 52 firms, 0 bucket drifts vs v3.58)

[2026-04-29] v3.75: VERIFIED MECHANISM via DEF 14A — DGCL §266 conversion. Annual meeting April 24, 2026. 159,268,414 shares outstanding (record date Feb 27, 2026). Notable: New York State Common Retirement Fund publicly OPPOSED. Vote outcome (8-K Item 5.07) pending review.

Related firms

← Back to The Reincorporation Tracker · Cohort event study · JSON for EXPI