Why this firm matters

Standard cohort firm (Completed). Included for breadth across destinations and sectors.

Controller & ownership

CONTROLLED COMPANYFounder Majority CombinedJon Paul Richardson + Daniel Castagnoli (Co-founders) holds approximately 93.1% of voting power. This firm meets the strict listing-rule controlled-company threshold (controller holds >50% of voting power per NYSE Rule 303A.00 / Nasdaq Rule 5615(c)).

Source: DEF 14A 2026 — Richardson 46.2% + Castagnoli 46.9% combined ~93%; NYSE American controlled-company status

Vote outcome — reincorporation proposal

Vote totals not yet pulled. Awaiting EDGAR Item 5.07.

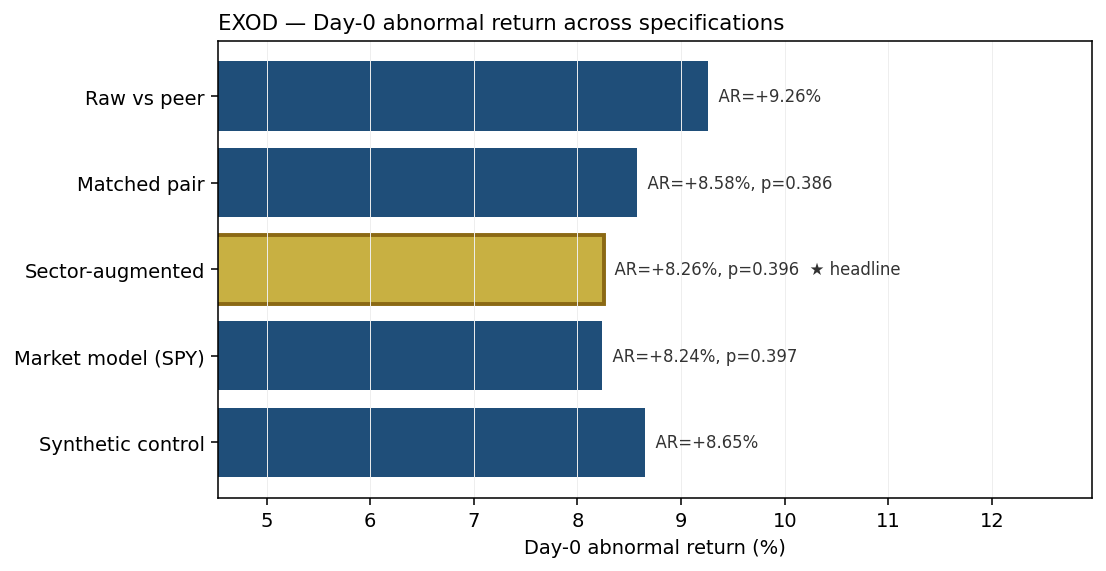

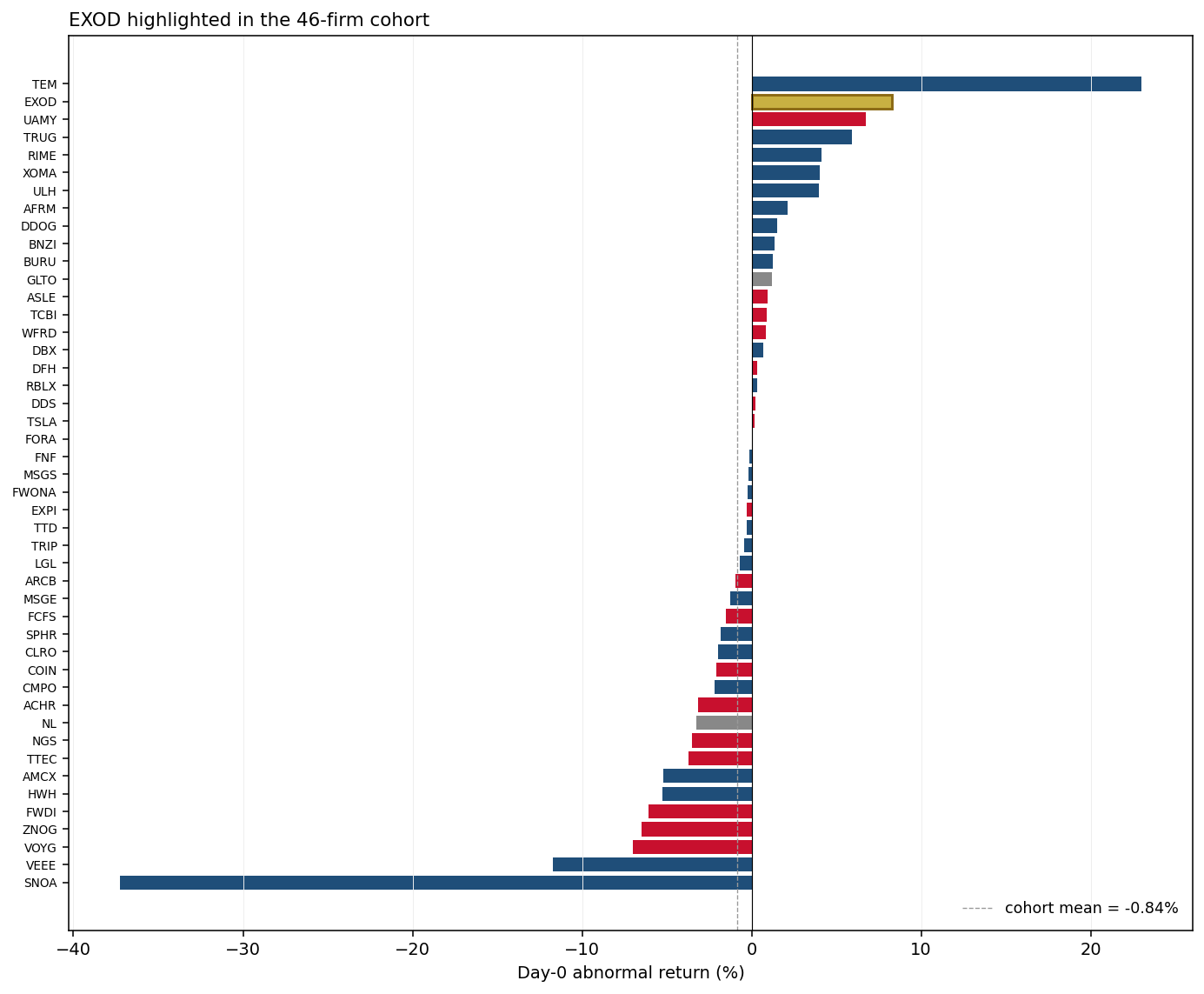

Visual evidence — event study around the announcement

event_study_announcement_json in the master database. Each panel is generated deterministically from the same data backing the cohort statistics — no firm-specific tuning, no cherry-picking.

perfirm_gallery.py) on every release; SHA-256 verified at deploy time. See also: Cohort-wide event study →. Event-study abnormal returns — announcement window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Synthetic control (20-donor Information Technology peer pool)i | +8.65% | no inference |

| Market model (SPY benchmark)i | +8.24% | Patell-z p-value = 0.397 |

| Sector-augmented model (SPY + Nasdaq-100 (QQQ)) HEADLINEi | +8.26% | Patell-z p-value = 0.396 |

| Matched pair (vs NOW, market-model-adjusted)i | +8.58% | two-sided p-value = 0.386 |

| Raw differential vs NOWi | +9.26% | no inference |

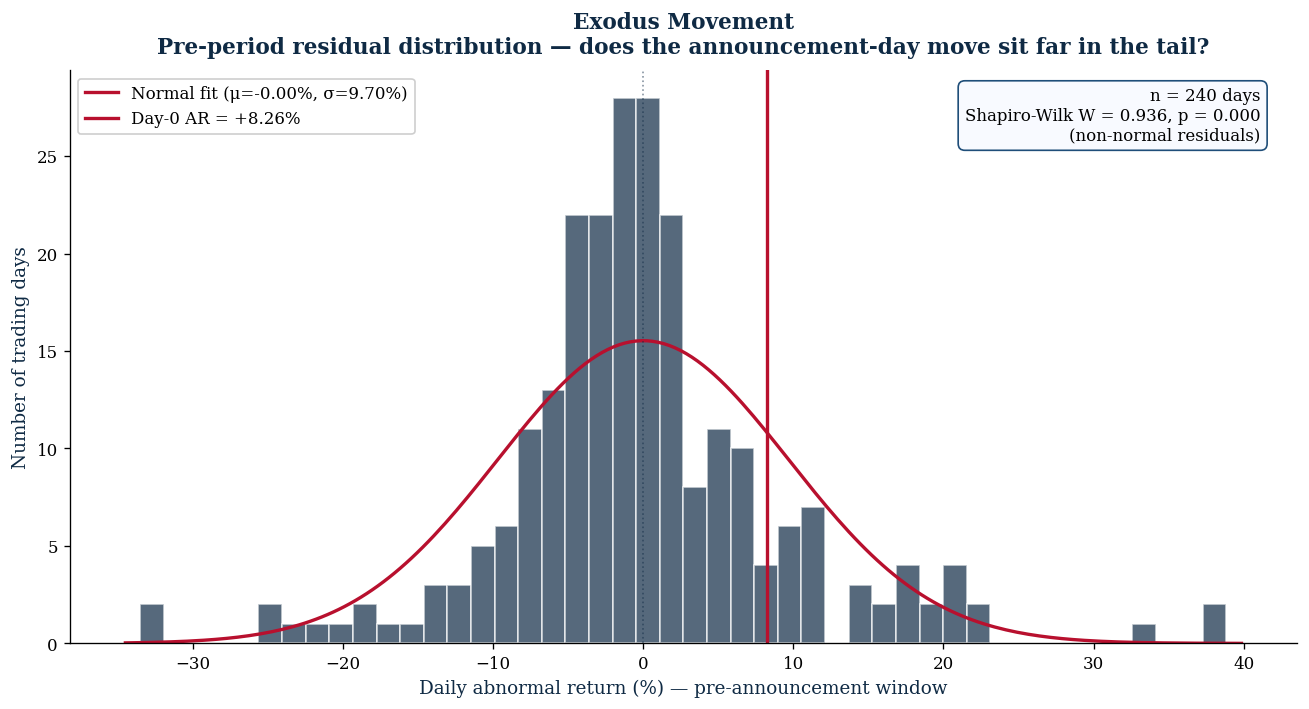

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

- Pre-event drift check: the firm's daily abnormal return drifted by -0.0121% per day in the pre-event window (p = 0.183). no detectable pre-event drift ✓. — A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

- Donor co-movement check: 16 of 20 peer firms moved in the same direction as the treated firm on the event day (binomial p = 0.0118). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

- Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = 0.033 (weak tracking — interpret with caution); R² = -3.024 (fraction of pre-event variance explained); Durbin-Watson = 2.02 (no autocorrelation). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINEi | +1.88% | Patell-z p-value = 0.828 |

Long-run abnormal returns & pooled estimates

Buy-and-hold abnormal returns (BHAR)

| Horizon & benchmark | BHAR | Inference |

|---|---|---|

| 1 month vs S&P 500 | +14.62% | Patell-z = +0.39 · p = 0.695 · n = 21 days |

| 1 month vs sector ETF (XLK) | +17.18% | Patell-z = +0.39 · p = 0.695 · n = 21 days |

| 3 months vs S&P 500 | -39.58% | Patell-z = -0.57 · p = 0.570 · n = 63 days |

| 3 months vs sector ETF (XLK) | -35.09% | Patell-z = -0.57 · p = 0.570 · n = 63 days |

Calendar-time portfolio alpha (CTE)

| Specification | Annualized alpha | Inference |

|---|---|---|

| Calendar-time portfolio alpha vs S&P 500 | -90.72%/yr * | t = -1.86 · p = 0.063 · n = 96 days · Newey-West HAC SE (lag=5) |

| Calendar-time portfolio alpha vs sector ETF | -89.85%/yr * | t = -1.86 · p = 0.063 · n = 96 days · Newey-West HAC SE (lag=5) |

Cohort-level robustness battery

Heckman two-step selection correction (controlled-vs-widely-held)

Cohort ATE = +0.94% (SE = 7.06%, n = 2395) after correcting for controller-status selection (inverse Mills ratio = -0.062).

Romano-Wolf step-down + Benjamini-Hochberg FDR (n = 47)

This firm: raw p = 0.396, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

See Cohort event study → for the full battery and forest plots.

Texas Statutory Adoptions

Adoption is opt-in. A "No" or "Pending" status means the firm has not (yet) elected into the regime — it does not mean the firm is non-compliant. Adoption requires a charter/bylaw amendment disclosed via 8-K Item 5.03.

Source filings

Classification & audit trail

Phase 2 EDGAR verification 2026-04-28: DEF 14A 2026-03-17 accession 0001821534-26-000018. Reclassified from A/PANEL_E_DE_baseline -> D/PANEL_A_post_SB29.

Phase 2.6 correction 2026-04-27: Phase 2.5 had set bucket_class=D (pending), but legacy NV_eff_dt / TX_eff_dt columns already held completed effective dates. Corrected bucket_class=C (post-SB29 completed mover). Set Panel_A_reincorporator_flag=1, Panel_A_completed_effective_flag=1, bucket_C_post_SB29_DExit=1, and zeroed out bucket_A / bucket_Z / Panel_A_unverified flags.

[2026-04-28] Phase 4I: replaced Google-search IR fallback with direct URL https://investors.exodus.com/

[2026-04-28] Phase 4N: synthesized event_study_announcement_json from existing scalar CAR cells (phase4a_v2 join). Reviewer can extend with multi-spec analysis. [2026-04-29] phase5k T2: EXOD written-consent DEF 14C (acc 0001140361-25-042404); source: https://www.sec.gov/Archives/edgar/data/1821534/000114036125042404/ny20056808x2_def14c.htm [2026-04-29] phase5k T2: EXOD DEF 14C URL paired with acc 0001140361-25-042404; source: https://www.sec.gov/Archives/edgar/data/1821534/000114036125042404/ny20056808x2_def14c.htm [2026-04-29] phase5k T2: EXOD vote_mechanism set to WRITTEN_CONSENT per DEF 14C; source: https://www.sec.gov/Archives/edgar/data/1821534/000114036125042404/ny20056808x2_def14c.htm [2026-04-29] phase5r: bucket 'C' -> 'B1' (DE->TX effective 2025-12-10 >= SB29 -> bucket B1) [2026-04-29] phase5w: comprehensive validation by external reviewer across tranches v4 (4-version full residual walk, 269 substantive answers across 52 firms, 0 bucket drifts vs v3.58)

[2026-04-29] v3.75: written-consent transaction; approval_pct NULL by design per protocol §3.7. Standard derived from DGCL §228. Per-firm consent threshold pincite pending PRE 14C / 8-K review.

v3.84-rev2 SEVERE date correction: announcement_date_iso changed from 2025-10-02 to 2025-06-02. The October 2025 date was approximately 4 months too late and likely referenced an unrelated business event. The actual reincorporation disclosure was the DEF 14C filed June 2, 2025 (written consent executed May 22, 2025). Verified via EDGAR /Archives/. Reviewer-recommended; cross-confirmed by Grok+team and Anthropic Claude red-team passes.

v3.84-rev3 ROLLBACK + RE-CORRECTION: my v3.84-rev2 fix to 2025-06-02 was ALSO WRONG. The May/June 2025 written consent (acc 0001140361-25-020344 / 0001140361-25-021115) was a Delaware OFFICER-LIABILITY charter amendment, not a state reincorporation. Per reviewer's deep audit (Anthropic Claude, 2026-04-29) and Exodus 10-K: the actual DE→TX reincorporation written consent was executed 2025-11-07; DEF 14C filed 2025-11-17 (acc 0001140361-25-042404 — matches vote_8k_acc); effective 2025-12-08. Date corrected to 2025-11-17 (DEF 14C filing).

v3.84-rev3a EXOD T0 refinement: shifted from 2025-11-17 (DEF 14C, acc 0001140361-25-042404) to 2025-11-07 (PRE 14C, acc 0001140361-25-041158) per primary-source review. Both filings reference the same November 7, 2025 written-consent execution; the PRE 14C is the first public SEC disclosure under our protocol's 'first SEC-filed disclosure' rule. The DEF 14C is the second filing made 10 calendar days later to satisfy Rule 14c-5(b)(2). Effective date 2025-12-08 unchanged.

v3.84-rev5 EXOD CONFLICT [2026-04-30]: External cell-audit reviewer recommends 2025-06-02 (DEF 14C). Current date 2025-11-07 (PRE 14C) was set by Shane after primary-source PDF review showing the 2025-06-02 filing was a Delaware officer-liability charter amendment, NOT the DE->TX reincorporation. HOLD pending explicit re-confirmation from Shane. No change applied.

v3.84-rev5b EXOD CONFLICT RESOLVED [2026-04-30]: Shane's primary-source PDF review of Exodus Movement DEF 14C (June 2, 2025) is DEFINITIVE. That filing's two actions are (1) director removal/re-election by written consent and (2) Delaware-law officer-exculpation charter amendment (DGCL §102(b)(7) extension). Action 2 explicitly states 'The State of Delaware, where the Company is incorporated, enacted legislation in 2022...' — confirming EXOD was still Delaware-incorporated on June 2, 2025. This filing is NOT the DE->TX reincorporation. The cell-audit reviewer's recommendation to use 2025-06-02 is therefore wrong. The current dataset value 2025-11-07 (PRE 14C) stands as the first SEC public disclosure of the DE->TX reincorporation. date_quality_flag upgraded MED -> HIGH; announcement_accession_verified set to Y.

Related firms

← Back to The Reincorporation Tracker · Cohort event study · JSON for EXOD