Why this firm matters

Destination is Cayman Islands — an outbound move to a non-TX/NV jurisdiction. Retained as a revealed-preference comparator (Y bucket) rather than included in completed-DExit counts.

Vote outcome — reincorporation proposal

Vote totals not yet pulled. Awaiting EDGAR Item 5.07.

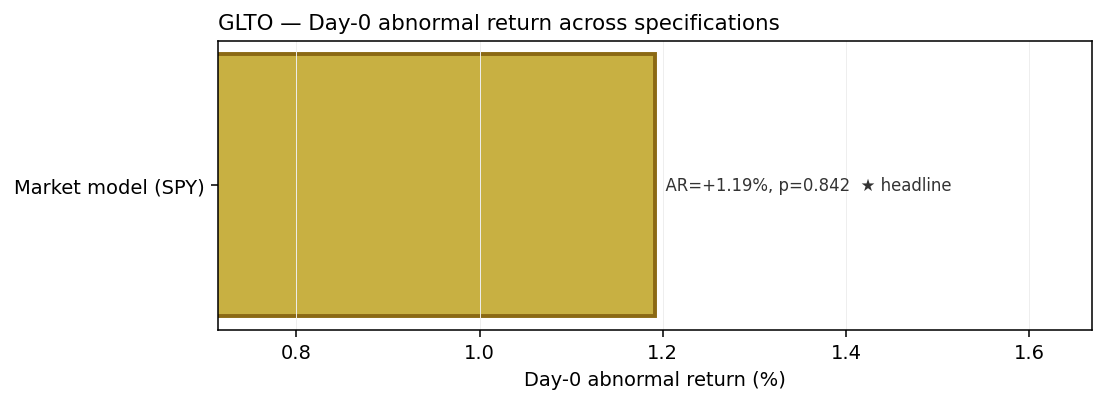

Visual evidence — event study around the announcement

event_study_announcement_json in the master database. Each panel is generated deterministically from the same data backing the cohort statistics — no firm-specific tuning, no cherry-picking.

perfirm_gallery.py) on every release; SHA-256 verified at deploy time. See also: Cohort-wide event study →. Event-study abnormal returns — announcement window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Market model (SPY benchmark) HEADLINEi | +1.19% | Patell-z p-value = 0.842 |

Event-study abnormal returns — vote window

| Specification | CAR / BHAR | Details |

|---|---|---|

| Cumulative abnormal return — vote windowi | +22.58% *** | event 2026-02-09 · Synthetic-control benchmark · p=0.048 |

*** p < 0.05 · * p < 0.10 · CAR = cumulative abnormal return; BHAR = buy-and-hold abnormal return; FFC6 = Fama-French five-factor + momentum (UMD)

Long-run abnormal returns & pooled estimates

No long-run / pooled estimates available for this firm yet — run phase5z_compute_longrun.py on Windows to populate (requires effective date ≥ 3 months ago).

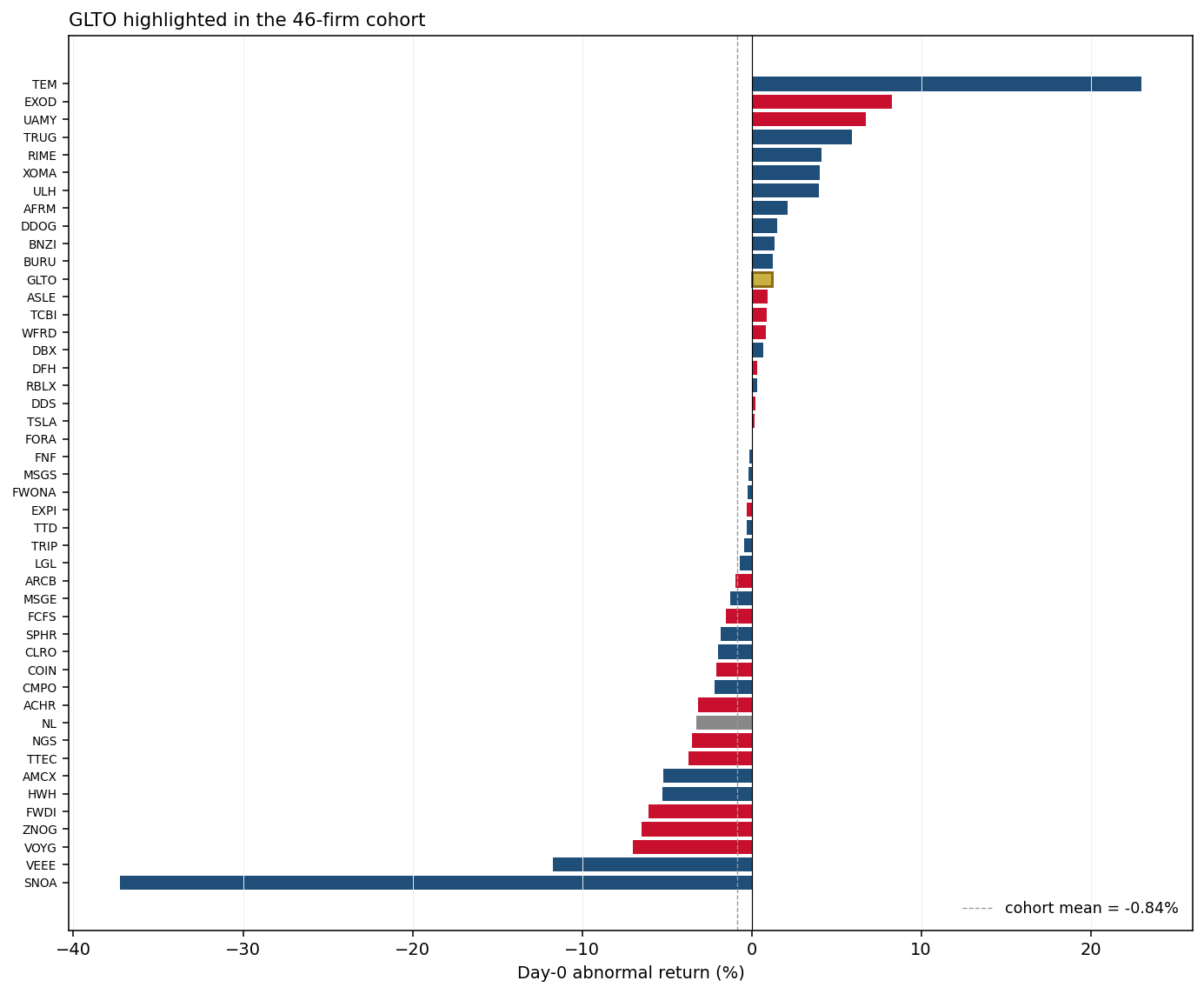

Cohort-level robustness battery

Heckman two-step selection correction (controlled-vs-widely-held)

Cohort ATE = +0.94% (SE = 7.06%, n = 2395) after correcting for controller-status selection (inverse Mills ratio = -0.062).

Romano-Wolf step-down + Benjamini-Hochberg FDR (n = 47)

This firm: raw p = 0.842, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

See Cohort event study → for the full battery and forest plots.

Source filings

Classification & audit trail

v2.9.2: outbound POST-SB29 to non-TX/NV destination; reclassified A→Z (out of SB29 scope per BLP corroboration)

v2.9.3: bucket_Y=1 (revealed-preference comparator: DE leaver post-SB29 to non-TX/NV destination)

[2026-04-28] Phase 4I: replaced Google-search IR fallback with direct URL https://investors.galecto.com/ [2026-04-29] phase5k T1: GLTO effective_missing -> 2026-02-09 from 8-K Item 5.03 (acc 0001193125-26-043741); source: https://www.sec.gov/Archives/edgar/data/1800315/000119312526043741/glto-20260206.htm [2026-04-29] phase5k T2: GLTO vote_source_8k from 8-K (acc 0001193125-26-043741); source: https://www.sec.gov/Archives/edgar/data/1800315/000119312526043741/glto-20260206.htm [2026-04-29] phase5k T2: GLTO vote_source_8k_url paired with acc 0001193125-26-043741; source: https://www.sec.gov/Archives/edgar/data/1800315/000119312526043741/glto-20260206.htm [2026-04-29] phase5w: comprehensive validation by external reviewer across tranches v3 (4-version full residual walk, 269 substantive answers across 52 firms, 0 bucket drifts vs v3.58) [2026-04-29] phase5x: Decision #1 per Shane 2026-04-29 -- Y-bucket firms (DE->non-TX/NV) remain in dashboard cohort (flag=1) as revealed-preference comparators; the 'why others left DE' question matters even if destination isn't TX or NV

[2026-04-29] v3.75: VERIFIED via 8-K — DELAWARE → CAYMAN ISLANDS (NOT TX/NV — comparator/Bucket Y, same class as CDT). Special meeting February 9, 2026 approved Cayman conversion + Series B/C conversion + 300M→500M authorized shares + 2026 equity plans. Rebranded to Damora Therapeutics (DMRA) March 10, 2026. Item 5.07 vote-tally pincite pending.

Related firms

← Back to The Reincorporation Tracker · Cohort event study · JSON for GLTO